import numpy as np

import pandas as pd

import statsmodels.api as sm

import statsmodels.formula.api as smf

import matplotlib.pyplot as plt9 Statistical Models

9.1 Introduction

Statistical modeling is a cornerstone of data science, offering tools to understand complex relationships within data and to make predictions. Python, with its rich ecosystem for data analysis, features the statsmodels package— a comprehensive library designed for statistical modeling, tests, and data exploration. statsmodels stands out for its focus on classical statistical models and compatibility with the Python scientific stack (numpy, scipy, pandas).

9.1.1 Installation of statsmodels

To start with statistical modeling, ensure statsmodels is installed:

Using pip:

pip install statsmodels9.1.2 Features of statsmodels

Package statsmodels offers a comprehensive range of statistical models and tests, making it a powerful tool for a wide array of data analysis tasks:

Linear Regression Models: Essential for predicting quantitative responses, these models form the backbone of many statistical analysis operations.

Generalized Linear Models (GLM): Expanding upon linear models, GLMs allow for response variables that have error distribution models other than a normal distribution, catering to a broader set of data characteristics.

Time Series Analysis: This includes models like ARIMA for analyzing and forecasting time-series data, as well as more complex state space models and seasonal decompositions.

Nonparametric Methods: For data that does not fit a standard distribution,

statsmodelsprovides tools like kernel density estimation and smoothing techniques.Statistical Tests: A suite of hypothesis testing tools allows users to rigorously evaluate their models and assumptions, including diagnostics for model evaluation.

Integrating statsmodels into your data science workflow enriches your analytical capabilities, allowing for both exploratory data analysis and complex statistical modeling.

9.2 Generalized Linear Models

Generalized Linear Models (GLM) extend the classical linear regression to accommodate response variables, that follow distributions other than the normal distribution. GLMs consist of three main components:

- Random Component: This specifies the distribution of the response variable \(Y\). It is assumed to be from the exponential family of distributions, such as Binomial for binary data and Poisson for count data.

- Systematic Component: This consists of the linear predictor, a linear combination of unknown parameters and explanatory variables. It is denoted as \(\eta = X\beta\), where \(X\) represents the explanatory variables, and \(\beta\) represents the coefficients.

- Link Function: The link function, \(g\), provides the relationship between the linear predictor and the mean of the distribution function. For a GLM, the mean of \(Y\) is related to the linear predictor through the link function as \(\mu = g^{-1}(\eta)\).

Generalized Linear Models (GLM) adapt to various data types through the selection of appropriate link functions and probability distributions. Here, we outline four special cases of GLM: normal regression, logistic regression, Poisson regression, and gamma regression.

- Normal Regression (Linear Regression). In normal regression, the response variable has a normal distribution. The identity link function (\(g(\mu) = \mu\)) is typically used, making this case equivalent to classical linear regression.

- Use Case: Modeling continuous data where residuals are normally distributed.

- Link Function: Identity (\(g(\mu) = \mu\))

- Distribution: Normal

- Logistic Regression. Logistic regression is used for binary response variables. It employs the logit link function to model the probability that an observation falls into one of two categories.

- Use Case: Binary outcomes (e.g., success/failure).

- Link Function: Logit (\(g(\mu) = \log\frac{\mu}{1-\mu}\))

- Distribution: Binomial

- Poisson Regression. Poisson regression models count data using the Poisson distribution. It’s ideal for modeling the rate at which events occur.

- Use Case: Count data, such as the number of occurrences of an event.

- Link Function: Log (\(g(\mu) = \log(\mu)\))

- Distribution: Poisson

- Gamma Regression. Gamma regression is suited for modeling positive continuous variables, especially when data are skewed and variance increases with the mean.

- Use Case: Positive continuous outcomes with non-constant variance.

- Link Function: Inverse (\(g(\mu) = \frac{1}{\mu}\))

- Distribution: Gamma

Each GLM variant addresses specific types of data and research questions, enabling precise modeling and inference based on the underlying data distribution.

9.3 Statistical Modeling with statsmodels

This section was written by Leon Nguyen.

9.3.1 Introduction

Hello! My name is Leon Nguyen (they/she) and I am a second-year undergraduate student studying Statistical Data Science and Mathematics at the University of Connecticut, aiming to graduate in Fall 2025. One of my long-term goals is to make the field of data science more accessible to marginalized communities and minority demographics. My research interests include data visualization and design. Statistical modeling is one of the most fundamental skills required for data science, and it’s important to have a solid understanding of how models work for interpretable results.

The statsmodels Python package offers a diverse range of classes and functions tailored for estimating various statistical models, conducting statistical tests, and exploring statistical data. Each estimator provides an extensive array of result statistics, rigorously tested against established statistical packages to ensure accuracy. This presentation will focus on the practical applications of the statistical modeling aspect.

9.3.2 Key Features and Capabilities

Some key features and capabilities of statsmodels are:

- Generalized Linear Models

- Diagnostic Tests

- Nonparametric methods

In this presentation, we will work with practical applications of statistical modeling in statsmodels. We will briefly cover how to set up linear, logistic, and Poisson regression models, and touch upon kernel density estimation and diagnostics. By the end of this presentation, you should be able to understand how to use statsmodels to analyze your own datasets using these fundamental techniques.

9.3.3 Installation and Setup

To install statsmodels, use pip install statsmodels or conda install statsmodels, depending on whether you are using pip or conda.

One of the major benefits of using statsmodels is their compatability with other commnonly used packages, such as NumPy, SciPy, and Pandas. These packages provide foundational scientific computing functionalities that are crucial for working with statsmodels. To ensure everything is set up correctly, import the necessary libraries at the beginning of your script:

Here are some minimum dependencies:

- Python >= 3.8

- NumPy >= 1.18

- SciPy >= 1.4

- Pandas >= 1.0

- Patsy >= 0.5.2

The last item listed above, patsy, is a Python library that provides simple syntax for specifying statistical models in Python. It allows users to define linear models using a formula syntax similar to the formulas used in R and other statistical software. More patsy documentation can be found here. This library is not used this demonstration, but is still worth noting.

9.3.4 Importing Data

There are a few different options to import data. For example, statsmodels documentation demonstrates how to importing from a CSV file hosted online from the Rdatasets repository:

# Reads the 'avocado' dataset from the causaldata package into df

df0 = sm.datasets.get_rdataset(dataname='avocado', package="causaldata").data

# We will be using this dataset later!

# Print out the first five rows of our dataframe

print(df0.head()) Date AveragePrice TotalVolume

0 2015-12-27 0.90 5040365.47

1 2015-12-20 0.94 4695737.21

2 2015-12-13 0.87 5259354.30

3 2015-12-06 0.78 5775536.27

4 2015-11-29 0.91 4575710.62We can also read directly from a local CSV file with pandas. For example, we will be using the NYC 311 request rodent data:

# Reads the csv file into df

df = pd.read_csv('data/rodent_2022-2023.csv')

# Brief data pre-processing

# Time reformatting

df['Created Date'] = pd.to_datetime(df['Created Date'], format = "%m/%d/%Y %I:%M:%S %p")

df['Closed Date'] = pd.to_datetime(df['Closed Date'], format = "%m/%d/%Y %I:%M:%S %p")

df['Created Year'] = df['Created Date'].dt.year

df['Created Month'] = df['Created Date'].dt.month

# Response time

df['Response Time'] = df['Closed Date'] - df['Created Date']

df['Response Time'] = df['Response Time'].apply(lambda x: x.total_seconds() / 3600) # in hours

# Remove unspecified borough rows

df = df.drop(df[df['Borough']=='Unspecified'].index)

# Remove 'other' open data channel type rows

df = df.drop(df[df['Open Data Channel Type']=='OTHER'].index)

print(df.head()) Unique Key Created Date Closed Date Agency \

0 59893776 2023-12-31 23:05:41 2023-12-31 23:05:41 DOHMH

1 59887523 2023-12-31 22:19:22 2024-01-03 08:47:02 DOHMH

2 59891998 2023-12-31 22:03:12 2023-12-31 22:03:12 DOHMH

3 59887520 2023-12-31 21:13:02 2024-01-03 09:33:43 DOHMH

4 59889297 2023-12-31 20:50:10 NaT DOHMH

Agency Name Complaint Type Descriptor \

0 Department of Health and Mental Hygiene Rodent Rat Sighting

1 Department of Health and Mental Hygiene Rodent Rat Sighting

2 Department of Health and Mental Hygiene Rodent Rat Sighting

3 Department of Health and Mental Hygiene Rodent Mouse Sighting

4 Department of Health and Mental Hygiene Rodent Rat Sighting

Location Type Incident Zip Incident Address ... \

0 3+ Family Apt. Building 11216 265 PUTNAM AVENUE ...

1 Commercial Building 10028 1538 THIRD AVENUE ...

2 3+ Family Apt. Building 10458 2489 TIEBOUT AVENUE ...

3 3+ Family Apt. Building 11206 116 JEFFERSON STREET ...

4 1-2 Family Dwelling 11206 114 ELLERY STREET ...

Location Zip Codes Community Districts \

0 (40.683855196486164, -73.95164557951071) 17618.0 69.0

1 (40.77924175816874, -73.95368859796383) 10099.0 23.0

2 (40.861693023118924, -73.89499228560491) 10936.0 6.0

3 (40.69974221739347, -73.93073474327662) 17213.0 42.0

4 (40.69844506428295, -73.94858040356128) 17213.0 69.0

Borough Boundaries City Council Districts Police Precincts Police Precinct \

0 2.0 49.0 51.0 51.0

1 4.0 1.0 11.0 11.0

2 5.0 22.0 29.0 29.0

3 2.0 30.0 53.0 53.0

4 2.0 49.0 51.0 51.0

Created Year Created Month Response Time

0 2023 12 0.000000

1 2023 12 58.461111

2 2023 12 0.000000

3 2023 12 60.344722

4 2023 12 NaN

[5 rows x 50 columns]9.3.5 Troubleshooting

Whenever you are having problems with statsmodels, you can access the official documentation by visiting this link. If you are working in a code editor, you can also run the following in a code cell:

sm.webdoc()

# Opens the official documentation page in your browserTo look for specific documentation, for example sm.GLS, you can run the following:

sm.webdoc(func=sm.GLS, stable=True)

# func : string* or function to search for documentation

# stable : (True) or development (False) documentation, default is stable

# *Searching via string has presented issues?9.3.6 Statistical Modeling and Analysis

Constructing statistical models with statsmodels generally follows a step-by-step process:

Import necessary libraries: This includes both

numpyandpandas, as well asstatsmodels.apiitself (sm).Load the data: This could be data from the

rdatasetrepository, local csv files, or other formats. In general, it’s best practice to load your data into apandasDataFrame so that it can easily be manipulated usingpandasfunctions.Prepare the data: This involves converting variables into appropriate types (e.g., categorical into factors), handling missing values, and creating appropriate interaction terms.

Define our model: what model is the appropriate representation of our research question? This could be an OLS regression (

sm.OLS), logistic regression (sm.Logit), or any number of other models depending on the nature of our data.Fit the model to our data: we use the

.fit()method which takes as input our dependent variable and independent variables.Analyze the results of the model: this is where we can get things like parameter estimates, standard errors, p-values, etc. We use the

.summary()method to print out these statistics.

9.3.7 Generalized Linear Models

GLM models allow us to construct a linear relationship between the response and predictors, even if their underlying relationship is not linear. This is done via a link function, which is a transformation which links the response variable to a linear model.

Key points of GLMs:

- Data should be independent and random.

- The response variable \(Y\) does not need to be normally distributed, but the distribution is from an exponential family (e.g. binomial, Poisson, normal).

- GLMs do not assume a linear relationship between the response variable and the explanatory variables, but assume a linear relationship between the transformed expected response in terms of the link function and the explanatory variables.

- GLMs are useful when the range of your response variable is constrained and/or the variance is not constant or normally distributed.

- GLM models transform the response variable to allow the fit to be done by least squares. The transformation done on the response variable is defined by the link function.

9.3.7.1 Linear Regression

Simple and muliple linear regression are special cases where the expected value of the dependent value is equal to a linear combination of predictors. In other words, the link function is the identity function \(g[E(Y)]=E(Y)\). Make sure assumptions for linear regression hold before proceeding. The model for linear regression is given by: \[y_i = X_i\beta + \epsilon_i\] where \(X_i\) is a vector of predictors for individual \(i\), and \(\beta\) is a vector of coefficients that define this linear combination.

We will be working with the avocado dataset from the package causaldata which contains information about the average price and total amount of avocados that were sold in California from 2015-2018. AveragePrice of a single avocado is our predictor, and TotalVolume is our outcome variable as a count of avocados.

Here is an application of SLR with statsmodels:

# We can use .get_rdataset() to load data into Python from a repositiory of R packages.

df1 = sm.datasets.get_rdataset('avocado', package="causaldata").data

# Fit regression model

results1 = smf.ols('TotalVolume ~ AveragePrice', data=df1).fit()

# Analyze results

print(results1.summary()) OLS Regression Results

==============================================================================

Dep. Variable: TotalVolume R-squared: 0.441

Model: OLS Adj. R-squared: 0.438

Method: Least Squares F-statistic: 132.0

Date: Wed, 01 May 2024 Prob (F-statistic): 7.04e-23

Time: 15:29:41 Log-Likelihood: -2550.3

No. Observations: 169 AIC: 5105.

Df Residuals: 167 BIC: 5111.

Df Model: 1

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

Intercept 9.655e+06 3.3e+05 29.222 0.000 9e+06 1.03e+07

AveragePrice -3.362e+06 2.93e+05 -11.487 0.000 -3.94e+06 -2.78e+06

==============================================================================

Omnibus: 50.253 Durbin-Watson: 0.993

Prob(Omnibus): 0.000 Jarque-Bera (JB): 165.135

Skew: 1.135 Prob(JB): 1.38e-36

Kurtosis: 7.278 Cond. No. 9.83

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.We can interpret some values:

- coef: the coefficient of

AveragePricetells us how much adding one unit ofAveragePricechanges the predicted value ofTotalVolume. An important interpretation is that ifAveragePricewas to increase by one unit, on average we could expectTotalVolumeto change by this coefficient based on this linear model. This makes sense since higher prices should result in a smaller amount of avocados sold. - P>|t|: p-value to test significant effect of the predictor on the response, compared to a significance level \(\alpha=0.05\). When this p-value \(\leq \alpha\), we would reject the null hypothesis that there is no effect of

AveragePriceonTotalVolume, and conclude thatAveragePricehas a statistically significant effect onTotalVolume. - R-squared: indicates the proportion of variance explained by the predictors (in this case just

AveragePrice). If it’s close to 1 then most of the variability inTotalVolumeis explained byAveragePrice, which is good! However, only about 44.1% of the variability is explained, so this model could use some improvement. - Prob (F-statistic): indicates whether or not the linear regression model provides a better fit to a dataset than a model with no predictors. Assuming a significance level of 0.05, we would reject the null hypothesis (model with just the intercept does just as well with a model with predictors) since our F-value probability is less than 0.05. We know that

AveragePricegives at least some significant information aboutTotalVolume. (This makes more sense in MLR where you are considering multiple predictors.) - Skew: measures asymmetry of a distribution, which can be positive, negative, or zero. If skewness is positive, the distribution is more skewed to the right; if negative, then to the left. We ideally want a skew value of zero in a normal distribution.

- Kurtosis: a measure of whether or not a distribution is heavy-tailed or light-tailed relative to a normal distribution. For a normal distribution, we expect a kurtosis of 3. If our kurtosis is greater than 3, there are more outliers on the tails. If less than 3, then there are less.

- Prob (Jarque-Bera): indicates whether or not the residuals are normally distributed, which is required for the OLS linear regression model. In this case the test rejects the null hypothesis that the residuals come from a normal distribution. This is concerning because non-normality can lead to misleading conclusions and incorrect standard errors.

9.3.7.2 Logistic Regression

Logistic regression is used when the response variable is binary. The response distribution is logistic which means it has support (input) on \((0,1)\) and

is invertible. The log-odds link function is defined as \(\log\left(\frac{\mu}{1-\mu}\right)\), where \(\mu\) is the predicted probability.

Here we have an example from our rodents dataset, where the response variable Under 3h indicates whether the response time for a 311 service request was under 3 hours. 1 indicates that the response time is less than 3 hours, and 0 indications greater than or equal to 3 hours. We are creating a logistic regression model that can be used to estimate the odds ratio of 311 requests having a response time under 3 hours based on Borough and Open Data Channel Type (method of how 311 service request was submitted) as predictors.

# Loaded the dataset in a previous cell as df

# Create binary variable

df['Under 3h'] = (df['Response Time'] < 3).astype(int)

# Convert the categorical variable to dummy variables

df = df.loc[:, ['Borough', 'Open Data Channel Type', 'Under 3h']]

df = pd.get_dummies(df, dtype = int)

# Remove reference dummy variables

df.drop(

columns=['Borough_QUEENS', 'Open Data Channel Type_MOBILE'],

axis=1,

inplace=True

)For this regression to run properly, we needed to create \(k-1\) dummy variables with \(k\) levels in a given predictor. Here we have two categorical variables that we used pd.get_dummies() function to change from a categorical variable into dummy variables. We then dropped one dummy variable level from each category: 'Borough_QUEENS' and 'Open Data Channel Type_MOBILE'.

# Drop all rows with NaN values

df.dropna(inplace = True)

# Fit the logistic regression model using statsmodels

Y = df['Under 3h']

X = sm.add_constant(df.drop(columns = 'Under 3h', axis=1))

# need to consider constant manually

logitmod = sm.Logit(Y, X)

result = logitmod.fit(maxiter=30)

# Summary of the fitted model

print(result.summary())Optimization terminated successfully.

Current function value: 0.616020

Iterations 5

Logit Regression Results

==============================================================================

Dep. Variable: Under 3h No. Observations: 82846

Model: Logit Df Residuals: 82839

Method: MLE Df Model: 6

Date: Wed, 01 May 2024 Pseudo R-squ.: 0.02459

Time: 15:29:42 Log-Likelihood: -51035.

converged: True LL-Null: -52321.

Covariance Type: nonrobust LLR p-value: 0.000

=================================================================================================

coef std err z P>|z| [0.025 0.975]

-------------------------------------------------------------------------------------------------

const 0.8691 0.022 39.662 0.000 0.826 0.912

Borough_BRONX 0.1051 0.029 3.644 0.000 0.049 0.162

Borough_BROOKLYN -0.4675 0.023 -20.232 0.000 -0.513 -0.422

Borough_MANHATTAN -0.7170 0.024 -29.892 0.000 -0.764 -0.670

Borough_STATEN ISLAND 0.0122 0.050 0.243 0.808 -0.086 0.110

Open Data Channel Type_ONLINE 0.2933 0.019 15.402 0.000 0.256 0.331

Open Data Channel Type_PHONE 0.4540 0.018 25.836 0.000 0.420 0.488

=================================================================================================coef: the coefficients of the independent variables in the logistic regression equation are interpreted a little bit differently than linear regression; for example, if

borough_MANHATTANincreases by one unit and all else is held constant, we expect the log odds to decrease by 0.7192 units. According to this model, we can expect it is less likely for response time to be under three hours for a 311 service request in Manhattan compared to Queens (reference level). On the other hand, ifborough_BRONXincreases by one unit and all else is held constant, we expect the log odds to increase by 0.1047 units. We can expect it is more likely for response time to be under three hours for a 311 service request in the Bronx compared to Queens. If we want to look at comparisons betweenOpen Data Channel Type, from this model, we can also see that 311 requests in the dataset that were submitted via phone call are more likely to have a response time under three hours compared to those that were submitted via mobile.Log-Likelihood: the natural logarithm of the Maximum Likelihood Estimation(MLE) function. MLE is the optimization process of finding the set of parameters that result in the best fit. Log-likelihood on its own doesn’t give us a lot of information, but comparing this value from two different models with the same number of predictors can be useful. Higher log-likelihood indicates a better fit.

LL-Null: the value of log-likelihood of the null model (model with no predictors, just intercept).

Pseudo R-squ.: similar but not exact equivalent to the R-squared value in Least Squares linear regression. This is also known as McFadden’s R-Squared, and is computed as \(1-\dfrac{L_1}{L_0}\), where \(L_0\) is the log-likelihood of the null model and \(L_1\) is that of the full model.

LLR p-value: the p-value of log-likelihood ratio test statistic comparing the full model to the null model. Assuming a significance level \(\alpha\) of 0.05, if this p-value \(\leq \alpha,\) then we reject the null hypothesis that the model is not significant. We reject the null hypothesis; thus we can conclude this model has predictors that are significant (non-zero coefficients).

Another example:

We will use the macrodata dataset directly from statsmodels, which contains information on macroeconomic indicators in the US across different quarters from 1959 to 2009, such as unemployment rate, inflation rate, real gross domestic product, etc. I have created a binary variable morethan5p that has a value of 1 when the unemployment rate is more than 5% in a given quarter, and is 0 when it is equal to or less than 5%. We are creating a logistic regression model that can be used to estimate the odds ratio of the unemployment rate being greater than 5% based on cpi (end-of-quarter consumer price index) and pop (end-of-quarter population) as predictors.

# df2 is an instance of a statsmodels dataset class

df2 = sm.datasets.macrodata.load_pandas()

# add binary variable

df2.data['morethan5p'] = (df2.data['unemp']>5).apply(lambda x:int(x))

# Subset data

df2 = df2.data[['morethan5p','cpi','pop']]

# Logit regression model

model = smf.logit("morethan5p ~ cpi + pop", df2)

result2 = model.fit()

summary = result2.summary()

print(summary)Optimization terminated successfully.

Current function value: 0.559029

Iterations 6

Logit Regression Results

==============================================================================

Dep. Variable: morethan5p No. Observations: 203

Model: Logit Df Residuals: 200

Method: MLE Df Model: 2

Date: Wed, 01 May 2024 Pseudo R-squ.: 0.05839

Time: 15:29:43 Log-Likelihood: -113.48

converged: True LL-Null: -120.52

Covariance Type: nonrobust LLR p-value: 0.0008785

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 24.0603 6.914 3.480 0.001 10.510 37.611

cpi 0.0744 0.023 3.291 0.001 0.030 0.119

pop -0.1286 0.038 -3.349 0.001 -0.204 -0.053

==============================================================================We can compute odds ratios and other information by calling methods on the fitted result object. Below are the 95% confidence intervals of the odds ratio \(e^{\text{coef}}\) of each coefficient:

odds_ratios = pd.DataFrame(

{

"Odds Ratio": result2.params,

"Lower CI": result2.conf_int()[0],

"Upper CI": result2.conf_int()[1],

}

)

odds_ratios = np.exp(odds_ratios)

print(odds_ratios) Odds Ratio Lower CI Upper CI

Intercept 2.813587e+10 36683.855503 2.157971e+16

cpi 1.077211e+00 1.030540 1.125997e+00

pop 8.793232e-01 0.815568 9.480629e-01Note these are no longer log odds we are looking at! We estimate with 95% confidence that the true odds ratio lies between the lower CI and upper CI for each coefficient. A larger odds ratio is associated with a larger probability that the unemployment rate is greater than 5%.

9.3.7.3 Poisson Regression

This type of regression is best suited for modeling the how the mean of a discrete variable depends on one or more predictors.

The log of the probability of success is modeled by:

\(\log(\mu) = b_0 + b_1x_1 + ... + b_kx_k\)

where \(\mu\) is the probability of success (the response variable). The intercept b0 is assumed to be 0 if not provided in the model. We will use .add_constant to indicate that our model includes an intercept term.

Let’s use the sunspots dataset from statsmodels. This is a one variable dataset that counts the number of sunspots that occur in a given year (from 1700 - 2008). Note that the link function for Poisson regression is a log function, which means \(\log{E(Y)}=X\beta.\)

We first load an instance of a statsmodels dataset class, analogous to a pandas dataframe:

df3 = sm.datasets.sunspots.load_pandas()

df3 = df3.data

df3['YEAR'] = df3['YEAR'].apply(lambda x: x-1700)

# YEAR is now number of years after 1700, scaling the data for better results

df3['YEAR2'] = df3['YEAR'].apply(lambda x: x**2)

# YEAR2 is YEAR squared, used as additional predictor

X = sm.add_constant(df3[['YEAR','YEAR2']])

# .add_constant indicates that our model includes an intercept term

Y = df3['SUNACTIVITY']

print(df3[['YEAR','YEAR2','SUNACTIVITY']].head()) YEAR YEAR2 SUNACTIVITY

0 0.0 0.0 5.0

1 1.0 1.0 11.0

2 2.0 4.0 16.0

3 3.0 9.0 23.0

4 4.0 16.0 36.0In the code above, we are altering our predictors a little bit from the orignal dataset; we are substracting the minimum year 1700 from all YEAR values so it is more centered. It is generally good practice to scale and center your data so that the model can have better fit. In our case this also aids the interpretability of the intercept coefficient we will see later. We are adding the varaible YEAR2, which is the number of years since 1700 squared to see if there is some non-linear relationship that may exist.

We can use the .GLM function with the family='poisson' argument to fit our model. Some important parameters:

data.endogacts as a series of observations for the dependent variable \(Y\)data.exogacts as a series of observations for each predictorfamilyspecifies the distribution appropriate for the model

result3 = sm.GLM(Y, X, family=sm.families.Poisson()).fit()

print(result3.summary()) Generalized Linear Model Regression Results

==============================================================================

Dep. Variable: SUNACTIVITY No. Observations: 309

Model: GLM Df Residuals: 306

Model Family: Poisson Df Model: 2

Link Function: Log Scale: 1.0000

Method: IRLS Log-Likelihood: -5548.3

Date: Wed, 01 May 2024 Deviance: 9460.6

Time: 15:29:43 Pearson chi2: 9.37e+03

No. Iterations: 5 Pseudo R-squ. (CS): 0.8057

Covariance Type: nonrobust

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 3.6781 0.026 140.479 0.000 3.627 3.729

YEAR 0.0003 0.000 0.747 0.455 -0.000 0.001

YEAR2 5.368e-06 1.13e-06 4.755 0.000 3.16e-06 7.58e-06

==============================================================================- coef: In this model, increasing the

YEARseems to increase the log of the expected count of Sunspot activity (SUNACTIVITY) by a small amount; the expected count of sunspot activty increases by \(e^{.0003}\) (note that increasingYEARalso increasesYEAR2so we have to be careful with interpretability!) This model also suggests that the number of sunspots is for the year 1700 is estimated to be \(e^{3.6781}\approx39.57\), while the number of actual sunspots that year was 5. - Deviance: two times the difference between the log-likelihood of a fitted GLM and the log-likelihood of a perfect model where fitted responses match observed responses. A greater deviance indicates a worse fit.

- Pearson chi2: measures the goodness-of-fit of the model based on the square deviations between observed and expected values based on the model. A large value suggests that the model does not fit well.

9.3.8 Diagnostic Tests

Throughout the GLMs listed above, we can find different statistics to assess how well the model fits the data. They include:

- Deviance: Measures the goodness-of-fit by taking the difference between the log-likelihood of a fitted GLM and the log-likelihood of a perfect model where fitted responses match observed responses. A larger deviance indicates a worse fit for the model. This is a test statistic for Likelihood-ratio tests compared to a chi-squared distribution with \(df=df_{\text{full}}-df_{\text{null}}\), for comparing a full model against a null model (or some reduced model) similar to a partial F-test.

print("Poisson Regression Deviance:", result3.deviance)Poisson Regression Deviance: 9460.616202027577- Pearson’s chi-square test: This tests whether the predicted probabilities from the model differ significantly from the observed counts. The test statistic is calculated by taking the difference between the null deviance (deviance of a model with just the intercept term) and residual deviance (how well the response variable can be predicted by a model with a given number of predictors). Large Pearson’s chi-squares indicate poor fit.

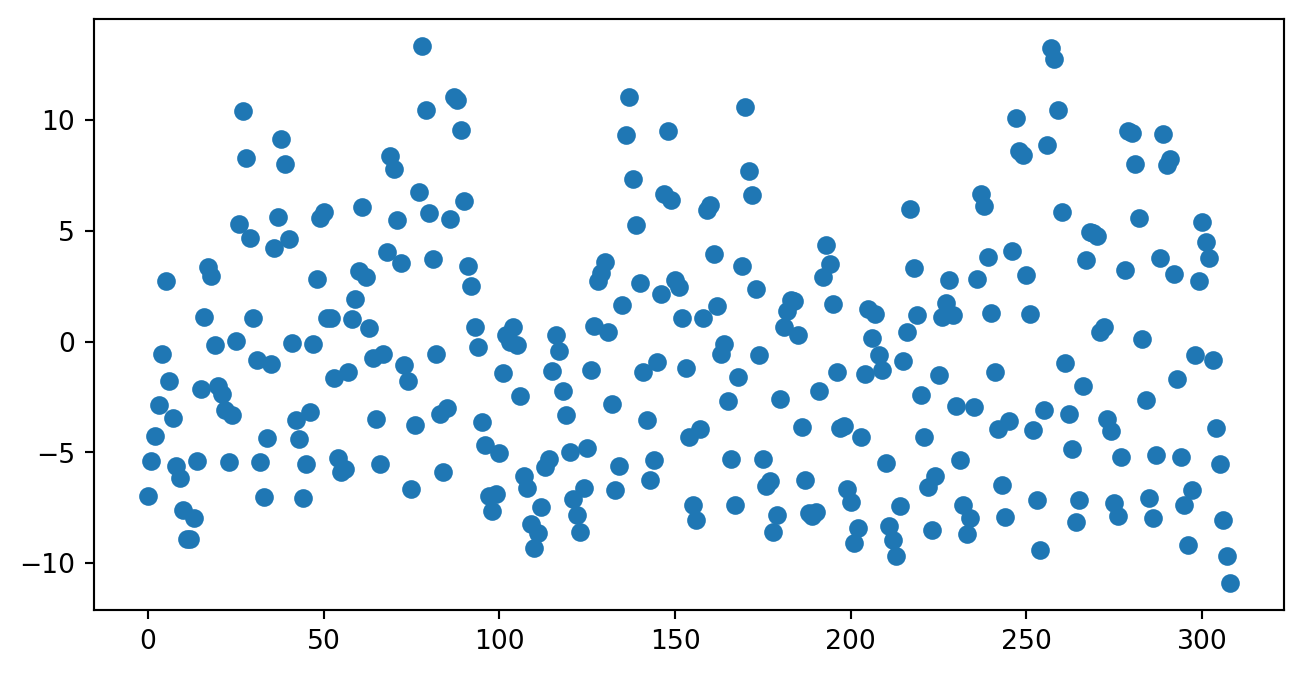

print("Chi Squared Stat:",result3.pearson_chi2)Chi Squared Stat: 9368.0333091202- Residual Plots: Like in linear regression, we can visually plot residuals to look for patterns that shouldn’t be there. There are different types of residuals that we can look at, such as deviance residuals:

fig = plt.figure(figsize=(8, 4))

plt.scatter(df3['YEAR'],result3.resid_deviance)

9.3.9 Nonparametric Models

9.3.9.1 Kernel Density Estimation

statsmodels has a non-parametric approach called kernel density estimation (KDE), which estimates the underlying probability of a given assortment of data points. KDE is used when you don’t have enough data points to form a parametric model. It estimates the density of continuous random variables, or extrapolates some continuous function from discrete counts. KDE is a non-parametric way to estimate the underlying distribution of data. The KDE weights all the distances of all data points relative to every location. The more data points there are at a given location, the higher the KDE estimate at that location. Points closer to a given location are generally weighted more than those further away. The shape of the kernel function itself indicates how the point distances are weighted. For example, a uniform kernel function will give equal weighting across all values within a bandwidth, whereas a triangle kernel function gives weighting dependent on linear distance.

KDE can be applied for univariate or multivariate data. statsmodels has two methods for this: - sm.nonparametric.KDEunivariate: For univariate data. This estimates the bandwidth using Scott’s rule unless specified otherwise. Much faster than using .KDEMultivariate due to its use of Fast Fourier Transforms on univariate, continuous data. - sm.nonparametric.KDEMultivariate: This applies to both univariate and multivariate data, but tends to be slower. Can use mixed types of data but requires specification.

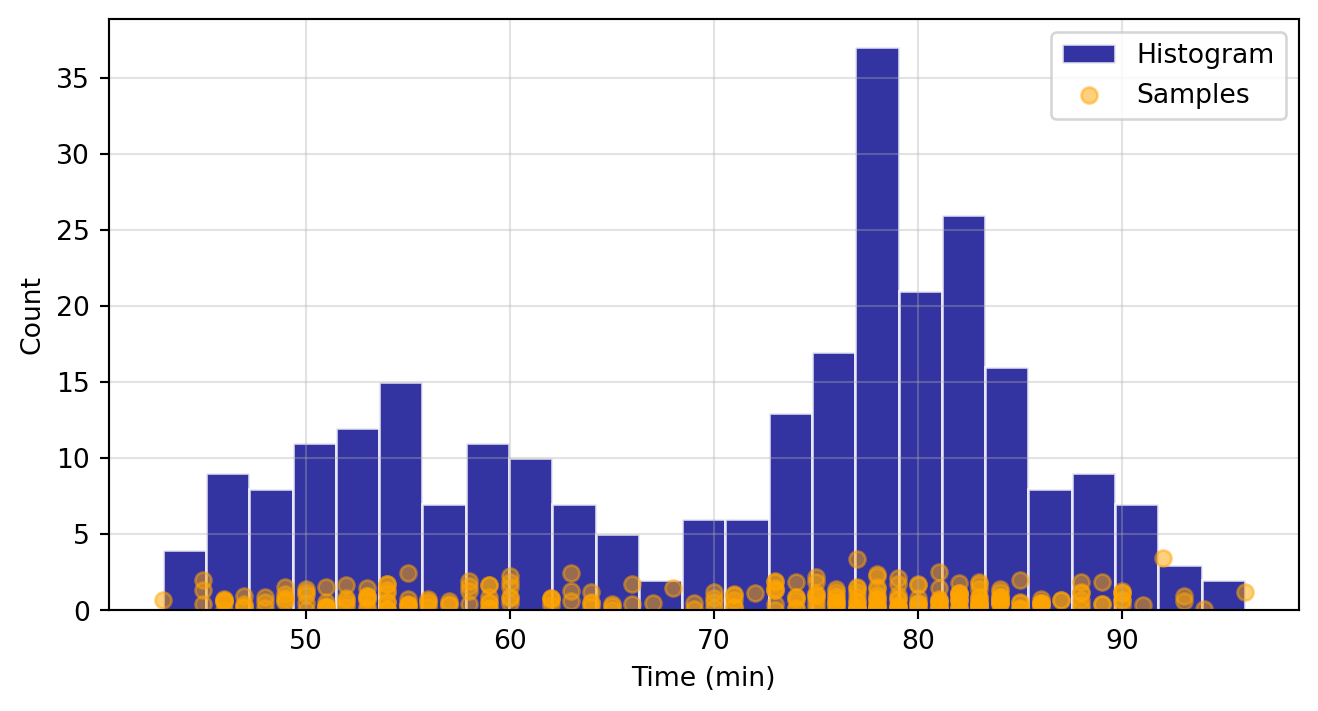

Here we will demonstrate how to apply it to univariate data, based off of examples provided in the documentation. We will generate a histogram of based off of geyser waiting time data from Rdatasets. This dataset records the waiting time between “Old Faithful” geyser’s eruptions in Yellowstone National Park. Our goal is to fit a KDE with a Gaussian kernel function to this data.

# Load data

df5 = sm.datasets.get_rdataset("faithful", "datasets")

waiting_obs = df5.data['waiting']

# Scatter plot of data samples and histogram

fig = plt.figure(figsize=(8, 4))

ax = fig.add_subplot()

ax.set_ylabel("Count")

ax.set_xlabel("Time (min)")

ax.hist(

waiting_obs,

bins=25,

color="darkblue",

edgecolor="w",

alpha=0.8,

label="Histogram"

)

ax.scatter(

waiting_obs,

np.abs(np.random.randn(waiting_obs.size)),

color="orange",

marker="o",

alpha=0.5,

label="Samples",

)

ax.legend(loc="best")

ax.grid(True, alpha=0.35)

Now we want to fit our KDE based on our waiting_obs sample:

kde = sm.nonparametric.KDEUnivariate(waiting_obs)

kde.fit() # Estimate the densities

print("Estimated Bandwidth:", kde.bw)

# Scatter plot of data samples and histogram

fig = plt.figure(figsize=(8, 4))

ax1 = fig.add_subplot()

ax1.set_ylabel("Count")

ax1.set_xlabel("Time (min)")

ax1.hist(

waiting_obs,

bins=25,

color="darkblue",

edgecolor="w",

alpha=0.8,

label="Histogram",

)

ax1.scatter(

waiting_obs,

np.abs(np.random.randn(waiting_obs.size)),

color="orange",

marker="o",

alpha=0.5,

label="Waiting times",

)

ax2 = ax1.twinx()

ax2.plot(

kde.support,

kde.density,

lw=3,

label="KDE")

ax2.set_ylabel("Density")

# Joining legends

lines, labels = ax1.get_legend_handles_labels()

lines2, labels2 = ax2.get_legend_handles_labels()

ax2.legend(lines + lines2, labels + labels2, loc=0)

ax1.grid(True, alpha=0.35)Estimated Bandwidth: 4.693019309795263

When fitting the KDE, a kde.bw or bandwidth parameter is returned. We can alter this to see how it affects the fit and smoothness of the curve. The smaller the bandwidth, the more jagged the estimated distribution becomes.

# Scatter plot of data samples and histogram

fig = plt.figure(figsize=(8, 4))

ax1 = fig.add_subplot()

ax1.set_ylabel("Count")

ax1.set_xlabel("Time (min)")

ax1.hist(

waiting_obs,

bins=25,

color="darkblue",

edgecolor="w",

alpha=0.8,

label="Histogram"

)

ax1.scatter(

waiting_obs,

np.abs(np.random.randn(waiting_obs.size)),

color="orange",

marker="o",

alpha=0.5,

label="Samples",

)

# Plot the KDE for various bandwidths

ax2 = ax1.twinx()

ax2.set_ylabel("Density")

for (bandwidth, color) in [(0.5,"cyan"), (4,"#bbaa00"), (8,"#ff79ff")]:

kde.fit(bw=bandwidth) # Estimate the densities

ax2.plot(

kde.support,

kde.density,

"--",

lw=2,

color=color,

label=f"KDE from samples, bw = {bandwidth}",

alpha=0.9

)

ax1.legend(loc="best")

ax2.legend(loc="best")

ax1.grid(True, alpha=0.35)

9.3.10 References

- Installing

statsmodels: Rdatasetsrepository andstatsmodelsdatasets:- https://github.com/vincentarelbundock/Rdatasets/blob/master/datasets.csv

- https://cran.r-project.org/web/packages/causaldata/causaldata.pdf

- https://hassavocadoboard.com/

- https://www.statsmodels.org/stable/datasets/index.html

- https://www.statsmodels.org/stable/datasets/generated/sunspots.html

- https://www.rdocumentation.org/packages/datasets/versions/3.6.2/topics/faithful

- NYC 311 Service Request Data:

- Getting help with

statsmodels: - Loading data, model fit, and summary procedure:

- Summary Data Interpretation:

- https://www.statology.org/a-simple-guide-to-understanding-the-f-test-of-overall-significance-in-regression/

- https://www.statology.org/linear-regression-p-value/

- https://www.statology.org/omnibus-test/

- https://www.statisticshowto.com/jarque-bera-test/

- https://www.statology.org/how-to-report-skewness-kurtosis/

- https://www.statology.org/interpret-log-likelihood/

- https://stackoverflow.com/questions/46700258/python-how-to-interpret-the-result-of-logistic-regression-by-sm-logit

- https://stats.oarc.ucla.edu/other/mult-pkg/faq/general/faq-what-are-pseudo-r-squareds/

- https://stats.oarc.ucla.edu/other/mult-pkg/faq/general/faq-how-do-i-interpret-odds-ratios-in-logistic-regression/

- https://vulstats.ucsd.edu/chi-squared.html

- https://roznn.github.io/GLM/sec-deviance.html

- Generalized Linear Models:

- Logistic Regression:

- https://www.andrewvillazon.com/logistic-regression-python-statsmodels/

- https://towardsdatascience.com/how-to-interpret-the-odds-ratio-with-categorical-variables-in-logistic-regression-5bb38e3fc6a8

- https://towardsdatascience.com/a-simple-interpretation-of-logistic-regression-coefficients-e3a40a62e8cf

- https://www.statology.org/interpret-log-likelihood/

- Poisson Regression:

- Non-parametric Methods:

- https://mathisonian.github.io/kde/

- https://www.statsmodels.org/stable/nonparametric.html

- https://www.statsmodels.org/dev/generated/statsmodels.nonparametric.kde.KDEUnivariate.html

- https://www.statsmodels.org/dev/generated/statsmodels.nonparametric.kernel_density.KDEMultivariate.html

- https://www.statsmodels.org/stable/examples/notebooks/generated/kernel_density.html

- Diagnostic tests:

- Data Visualization:

9.4 Time Series Analysis

This section is presented by Alex Pugh

9.4.1 What is Time Series Data?

Any information collected over regular intervals of time is considered to follow a time series. Time series analysis is a way of studying the characteristics of the response variable concerning time as the independent variable. To estimate the target variable in predicting or forecasting, using the time variable as the reference point can yield insights into trends, seasonal patterns, and future forecasts.

The opposite of time series data is cross-sectional data - where observations are collected at single point in time.

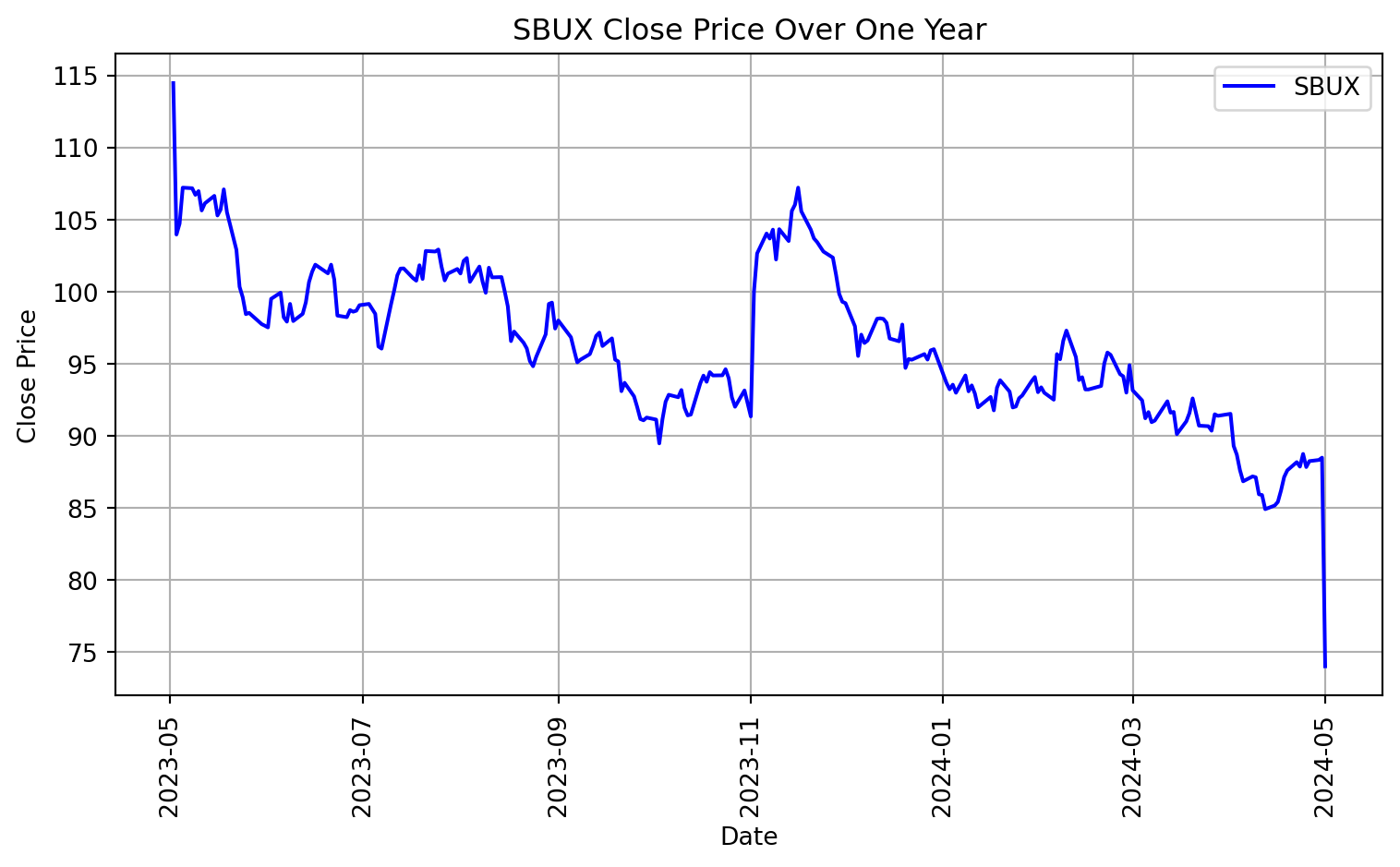

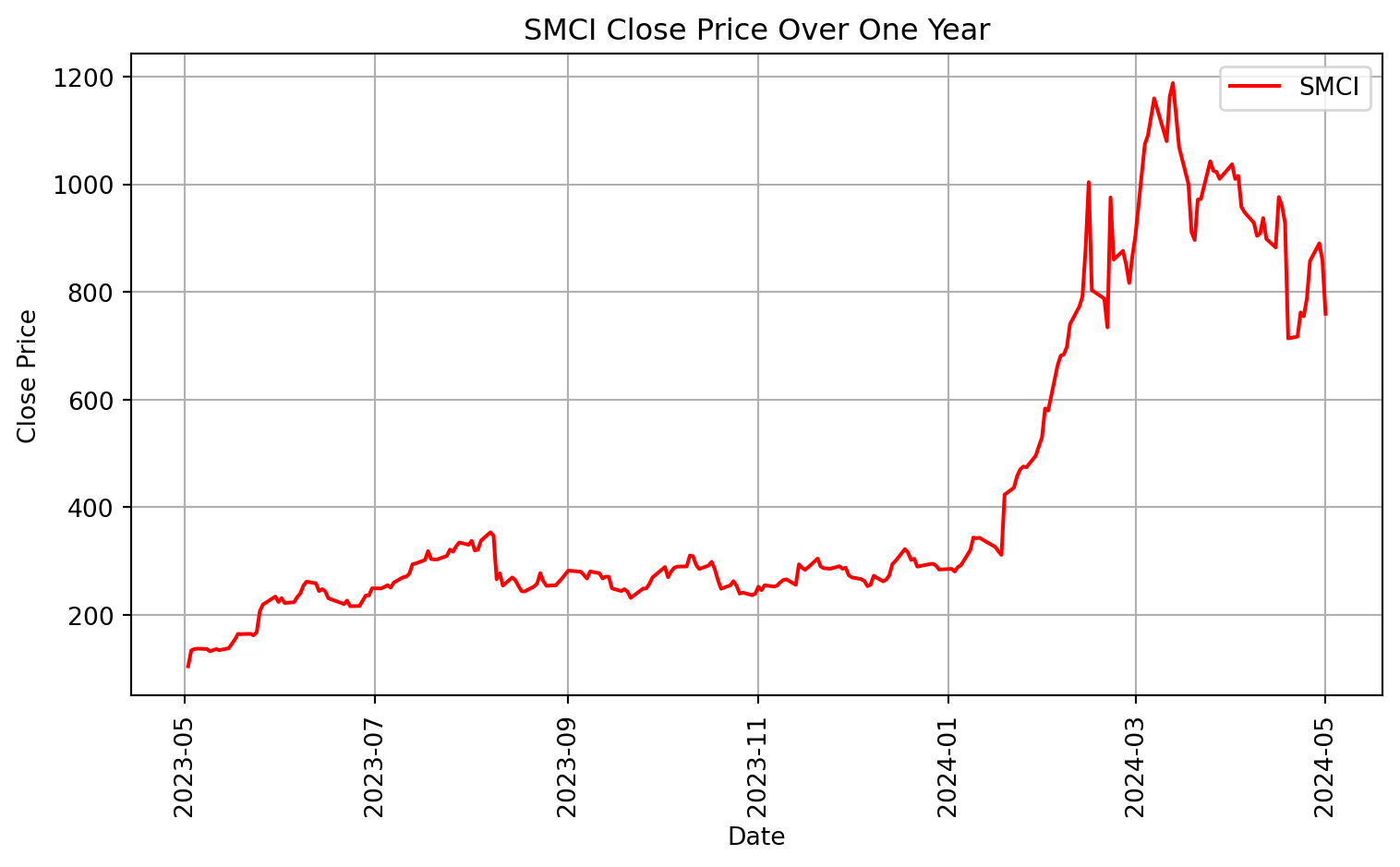

As an example of time series data, we will be using stock prices for two different companies: Starbucks (SBUX) and Supermicro (SMCI). Let’s vizualize their stock prices as a time series over the last year. We will pull real time data using the package yfinance.

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

import datetime

# Define the ticker symbols

tickerSymbol1 = 'SBUX'

tickerSymbol2 = 'SMCI'

# Get data for the past year

start_date = datetime.datetime.now() - datetime.timedelta(days=365)

end_date = datetime.datetime.now()

# Get the data

SBUX = yf.download(tickerSymbol1, start=start_date, end=end_date)

SMCI = yf.download(tickerSymbol2, start=start_date, end=end_date)

SBUX.dropna(subset=['Close'], inplace=True)

SMCI.dropna(subset=['Close'], inplace=True)

# Plotting SBUX data

plt.figure(figsize=(8, 5))

plt.plot(SBUX.index, SBUX['Close'], label='SBUX', color='blue')

plt.xlabel('Date')

plt.ylabel('Close Price')

plt.title('SBUX Close Price Over One Year')

plt.legend()

plt.grid(True)

plt.xticks(rotation=90)

plt.tight_layout()

plt.show()

# Plotting SMCI data

plt.figure(figsize=(8, 5))

plt.plot(SMCI.index, SMCI['Close'], label='SMCI', color='red')

plt.xlabel('Date')

plt.ylabel('Close Price')

plt.title('SMCI Close Price Over One Year')

plt.legend()

plt.grid(True)

plt.xticks(rotation=90)

plt.tight_layout()

plt.show()[*********************100%%**********************] 1 of 1 completed

[*********************100%%**********************] 1 of 1 completed

9.4.2 Identifying Data Trends

9.4.2.1 Elementary Data Trends

- Seasonal - regular or fixed interval shifts within the dataset in a continuous timeline

- Cyclical - no fixed interval, uncertainty in movement and its pattern

- Trend - no fixed interval nor any divergence within the given dataset is a continuous timeline

- Irregular - unexpected situations/events/scenarios and spikes in a short time span

9.4.2.2 Stationarity

Stationarity is the primary underlying assumption in most time series analysis. This refers to the idea that the origin of time does not affect the properties of the process under the statistical factor, and that the manner in which the data changes is constant. Statistically, this means that the unconditional joint probability distribution does not change when shifted in time. Consequently, parameters such as mean and variance also do not change over time. If you draw a line through the middle of a time series then it should be flat; it may have ‘seasonal’ cycles around the trend line, but overall it does not trend up nor down.

A stationary dataset should adhere to the following rules without having Trend, Seasonality, Cyclical, and Irregularity components of the time series.

- The mean value of them should be completely constant in the data during the analysis.

- The variance should be constant with respect to the time-frame.

- Covariance should measure the relationship between two variables and remain constant with resspect to time.

If any of these do not hold, we can say that the data is non-stationary.

We can use the Augmented Dickey-Fuller (ADF) Test or the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) Test to prove stationarity. The following are the null hypotheses for each test:

- Augmented Dickey-Fuller (ADF) Test:

- Null Hypothesis: The time series has a unit root, indicating it is non-stationary.

- Kwiatkowski-Phillips-Schmidt-Shin (KPSS) Test:

- Null Hypothesis: The time series is stationary around a deterministic trend.

from statsmodels.tsa.stattools import adfuller, kpss

import warnings

warnings.filterwarnings("ignore")

def adf_kpss_test(series, name):

# ADF Test

adf_result = adfuller(series, autolag='AIC')

print(f'ADF Test for {name}:')

print(f'ADF Statistic: {adf_result[0]}')

print(f'p-value: {adf_result[1]}')

print('Critical Values:')

for key, value in adf_result[4].items():

print(f' {key}: {value}')

# KPSS Test

kpss_result = kpss(series, regression='c')

print(f'\nKPSS Test for {name}:')

print(f'KPSS Statistic: {kpss_result[0]}')

print(f'p-value: {kpss_result[1]}')

print('Critical Values:')

for key, value in kpss_result[3].items():

print(f' {key}: {value}')

# Perform ADF and KPSS tests for SBUX

adf_kpss_test(SBUX['Close'], 'SBUX Stock Price')

# Perform ADF and KPSS tests for SMCI

adf_kpss_test(SMCI['Close'], 'SMCI Stock Price')ADF Test for SBUX Stock Price:

ADF Statistic: -1.8767488685364573

p-value: 0.34307697475147053

Critical Values:

1%: -3.4566744514553016

5%: -2.8731248767783426

10%: -2.5729436702592023

KPSS Test for SBUX Stock Price:

KPSS Statistic: 1.4362693363679242

p-value: 0.01

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739

ADF Test for SMCI Stock Price:

ADF Statistic: -0.8453696601714261

p-value: 0.80543059891859

Critical Values:

1%: -3.457437824930831

5%: -2.873459364726563

10%: -2.573122099570008

KPSS Test for SMCI Stock Price:

KPSS Statistic: 1.6523328114790083

p-value: 0.01

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.7399.4.2.2.1 Interpretation

Starbucks:

ADF Test: The ADF statistic is -1.84, and the p-value is 0.36. Since the p-value is greater than the significance level (0.05), we fail to reject the null hypothesis. This suggests that the time series of Starbucks’ stock price is non-stationary.

KPSS Test: The KPSS statistic is 1.29, and the p-value is 0.01. Here, since the p-value is less than the significance level (0.05), we reject the null hypothesis. This suggests that the time series of Starbucks’ stock price is non-stationary according to the KPSS test as well.

Supermicro:

ADF Test: The ADF statistic is -0.28, and the p-value is 0.93. Similar to Starbucks, the p-value is greater than the significance level (0.05), indicating non-stationarity.

KPSS Test: The KPSS statistic is 1.39, and the p-value is 0.01. Here, since the p-value is less than the significance level (0.05), we reject the null hypothesis. This suggests that the time series of Starbucks’ stock price is non-stationary according to the KPSS test as well.

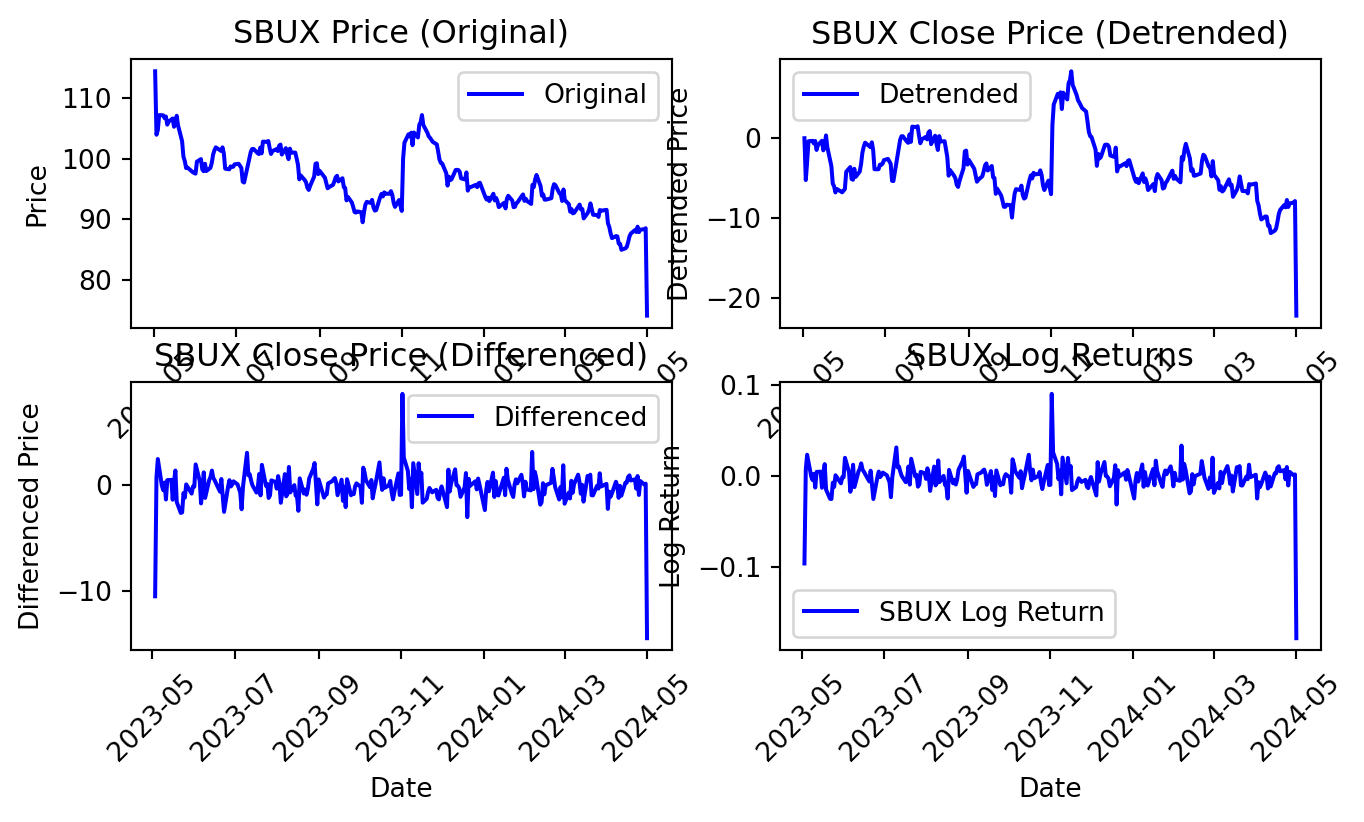

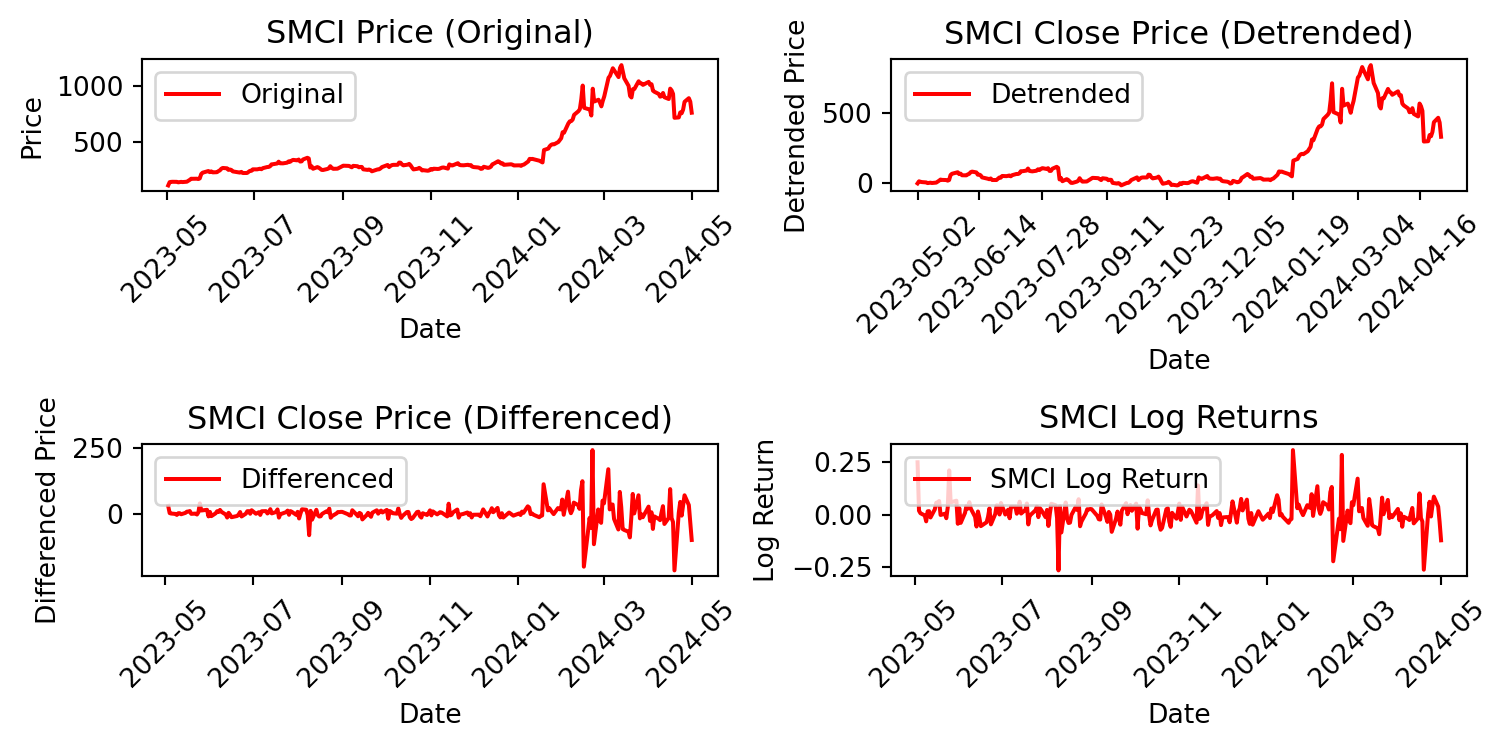

9.4.2.2.2 Converting Non-Stationary Into Stationary

There are three methods available for this conversion – detrending, differencing, and transformation.

Detrending

Detrending involves removing the trend effects from the given dataset and showing only the differences in values from the trend. It always allows cyclical patterns to be identified.

\[ Detrend(t) = Observation(t) - Rolling Mean of Observation(1,...,t) \]

Differencing

This is a simple transformation of the series into a new time series, which we use to remove the series dependence on time and stabilize the mean of the time series, so trend and seasonality are reduced during this transformation.

\[ Difference(t) = Observation(t) - Observation(t-1) \]

Transformation

Power transformations, square root transformations, and log tranformations are different possible methods. The most commonly used is a log transformation.

\[ Log Return(t) = log( Observation(t−1) / Observation(t) ) \]

import numpy as np

SBUX.reset_index(inplace=True)

SMCI.reset_index(inplace=True)

# Step 1: Detrending

SBUX['Detrended_Close'] = SBUX['Close'] - SBUX['Close'].rolling(window=365,

min_periods=1).mean()

SMCI['Detrended_Close'] = SMCI['Close'] - SMCI['Close'].rolling(window=365,

min_periods=1).mean()

# Step 2: Differencing

SBUX['Differenced_Close'] = SBUX['Close'].diff()

SMCI['Differenced_Close'] = SMCI['Close'].diff()

# Step 3: Log Return Transformation

# Calculate the percentage change

SBUX['Return'] = SBUX['Close'].pct_change()

SMCI['Return'] = SMCI['Close'].pct_change()

# Apply natural logarithm to the percentage change

SBUX['Log_Return'] = np.log(1 + SBUX['Return'])

SMCI['Log_Return'] = np.log(1 + SMCI['Return'])

# Plot original and transformed data for SBUX

plt.figure(figsize=(8, 4))

plt.subplot(2, 2, 1)

plt.plot(SBUX['Date'], SBUX['Close'], label='Original', color='blue')

plt.title('SBUX Price (Original)')

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend()

plt.xticks(rotation=45)

plt.subplot(2, 2, 2)

plt.plot(SBUX['Date'], SBUX['Detrended_Close'], label='Detrended',

color='blue')

plt.title('SBUX Close Price (Detrended)')

plt.xlabel('Date')

plt.ylabel('Detrended Price')

plt.legend()

plt.xticks(rotation=45)

plt.subplot(2, 2, 3)

plt.plot(SBUX['Date'][1:], SBUX['Differenced_Close'][1:],

label='Differenced', color='blue')

plt.title('SBUX Close Price (Differenced)')

plt.xlabel('Date')

plt.ylabel('Differenced Price')

plt.legend()

plt.xticks(rotation=45)

plt.subplot(2, 2, 4)

plt.plot(SBUX['Date'], SBUX['Log_Return'], label='SBUX Log Return',

color='blue')

plt.title('SBUX Log Returns')

plt.xlabel('Date')

plt.ylabel('Log Return')

plt.legend()

plt.xticks(rotation=45)

# Plot original and transformed data for SMCI

plt.figure(figsize=(8, 4))

plt.subplot(2, 2, 1)

plt.plot(SMCI['Date'], SMCI['Close'], label='Original', color = 'red')

plt.title('SMCI Price (Original)')

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend()

plt.xticks(rotation=45)

plt.subplot(2, 2, 2)

plt.plot(SMCI['Date'], SMCI['Detrended_Close'], label='Detrended',

color = 'red')

plt.title('SMCI Close Price (Detrended)')

plt.xlabel('Date')

plt.ylabel('Detrended Price')

plt.legend()

plt.xticks(SMCI['Date'][::30], rotation=45)

plt.subplot(2, 2, 3)

plt.plot(SMCI['Date'], SMCI['Differenced_Close'], label='Differenced',

color = 'red')

plt.title('SMCI Close Price (Differenced)')

plt.xlabel('Date')

plt.ylabel('Differenced Price')

plt.legend()

plt.xticks(rotation=45)

plt.subplot(2, 2, 4)

plt.plot(SMCI['Date'], SMCI['Log_Return'], label='SMCI Log Return',

color='red')

plt.title('SMCI Log Returns')

plt.xlabel('Date')

plt.ylabel('Log Return')

plt.legend()

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

We can now perform ADF and KPSS tests for stationarity on the changed data.

# Perform ADF and KPSS tests for SBUX

for series_name in ['Detrended_Close', 'Differenced_Close', 'Log_Return']:

adf_kpss_test(SBUX[series_name].dropna(), f"SBUX {series_name}")

# Perform ADF and KPSS tests for SMCI

for series_name in ['Detrended_Close', 'Differenced_Close', 'Log_Return']:

adf_kpss_test(SMCI[series_name].dropna(), f"SMCI {series_name}")ADF Test for SBUX Detrended_Close:

ADF Statistic: -1.4073562618808706

p-value: 0.578744397126715

Critical Values:

1%: -3.4566744514553016

5%: -2.8731248767783426

10%: -2.5729436702592023

KPSS Test for SBUX Detrended_Close:

KPSS Statistic: 0.5271824191729886

p-value: 0.03554450018626383

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739

ADF Test for SBUX Differenced_Close:

ADF Statistic: -14.000936609212907

p-value: 3.8632262739840877e-26

Critical Values:

1%: -3.456780859712

5%: -2.8731715065600003

10%: -2.572968544

KPSS Test for SBUX Differenced_Close:

KPSS Statistic: 0.11652570915449154

p-value: 0.1

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739

ADF Test for SBUX Log_Return:

ADF Statistic: -12.7194485598207

p-value: 9.900033390267044e-24

Critical Values:

1%: -3.456780859712

5%: -2.8731715065600003

10%: -2.572968544

KPSS Test for SBUX Log_Return:

KPSS Statistic: 0.1349413283134889

p-value: 0.1

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739

ADF Test for SMCI Detrended_Close:

ADF Statistic: -1.139124220886117

p-value: 0.6992202160005194

Critical Values:

1%: -3.457437824930831

5%: -2.873459364726563

10%: -2.573122099570008

KPSS Test for SMCI Detrended_Close:

KPSS Statistic: 1.4239792155349653

p-value: 0.01

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739

ADF Test for SMCI Differenced_Close:

ADF Statistic: -5.304547916944405

p-value: 5.358118355248533e-06

Critical Values:

1%: -3.457437824930831

5%: -2.873459364726563

10%: -2.573122099570008

KPSS Test for SMCI Differenced_Close:

KPSS Statistic: 0.11656499714929217

p-value: 0.1

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739

ADF Test for SMCI Log_Return:

ADF Statistic: -4.962303571332611

p-value: 2.6338728093037678e-05

Critical Values:

1%: -3.457437824930831

5%: -2.873459364726563

10%: -2.573122099570008

KPSS Test for SMCI Log_Return:

KPSS Statistic: 0.17570697728897325

p-value: 0.1

Critical Values:

10%: 0.347

5%: 0.463

2.5%: 0.574

1%: 0.739As of April 1, 2024, here is a summary table with the result of the above tests:

| Series | ADF Statistic | ADF p-value | KPSS Statistic | KPSS p-value | ADF H0 Rejected (Stationarity) | KPSS H0 Rejected (Stationarity) |

|---|---|---|---|---|---|---|

| SBUX Detrended_Close | -2.881 | 0.048 | 0.330 | 0.1 | No (Non-Stationary) | No (Stationary) |

| SBUX Differenced_Close | -6.864 | 1.57e-09 | 0.029 | 0.1 | Yes (Stationary) | No (Stationary) |

| SBUX Log_Return | -8.689 | 4.10e-14 | 0.029 | 0.1 | Yes (Stationary) | No (Stationary) |

| SMCI Detrended_Close | -0.733 | 0.838 | 1.161 | 0.01 | No (Non-Stationary) | Yes (Non-Stationary) |

| SMCI Differenced_Close | -2.761 | 0.064 | 0.365 | 0.092 | No (Non-Stationary) | No (Stationary) |

| SMCI Log_Return | -9.839 | 4.80e-17 | 0.157 | 0.1 | Yes (Stationary) | No (Stationary) |

The Starbucks stock price is stationary once differenced or the log return is taken, and the Supermicro stock price is approximately stationary once taken the log return.

9.4.2.3 Autocorrelation

Autocorrelation measures the relationship between a variable’s current value and its past values at different time lags. Data with strong autocorrelation indicates that current values are highly influenced from past values. The prescence of strong autocorrelation can lead to greater predicability of future values.

Autocorrelation coefficient for different time lags for a variable can be used to answer the following questions about a time series:

- Is the data random?

If a series is random, the autocorrelation between successive values at any time lag k are close to zero. This means that successive values of a time series are not related to each other.

- Does the data have a trend or is it stationary?

If a series has a trend, successive observations are highly correlated, and the autocorrelation coefficients typically are significantly different from zero for the first several time lags and then gradually drop toward zero as the number of lags increase.

- Is the data seasonal?

If a series has a seasonal pattern, a significant autocorrelation coefficient will occur at the seasonal time lag or multiples of the seasonal lag. The seasonal lag is 4 for quarterly data and 12 for monthly data.

The autocorrelation coefficients for a stationary series decline to zero fairly rapidly, generally after the second or third time lag. On the other hand, sample autocorrelation for nonstationary series remain fairly large for several time periods. Often, to analyze nonstationary series, the trend is removed before additional modeling occurs. This is the reasoning for performing the previous data manipulation.

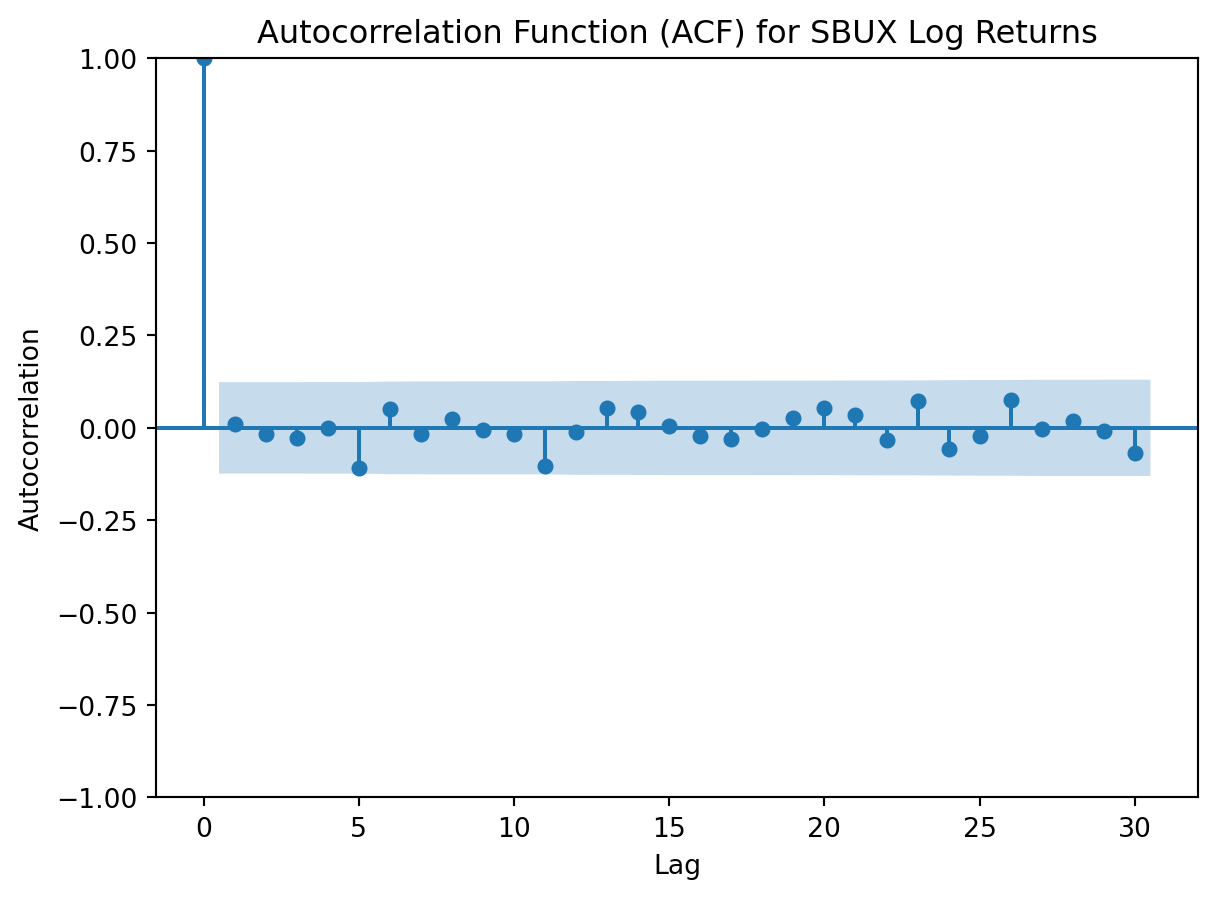

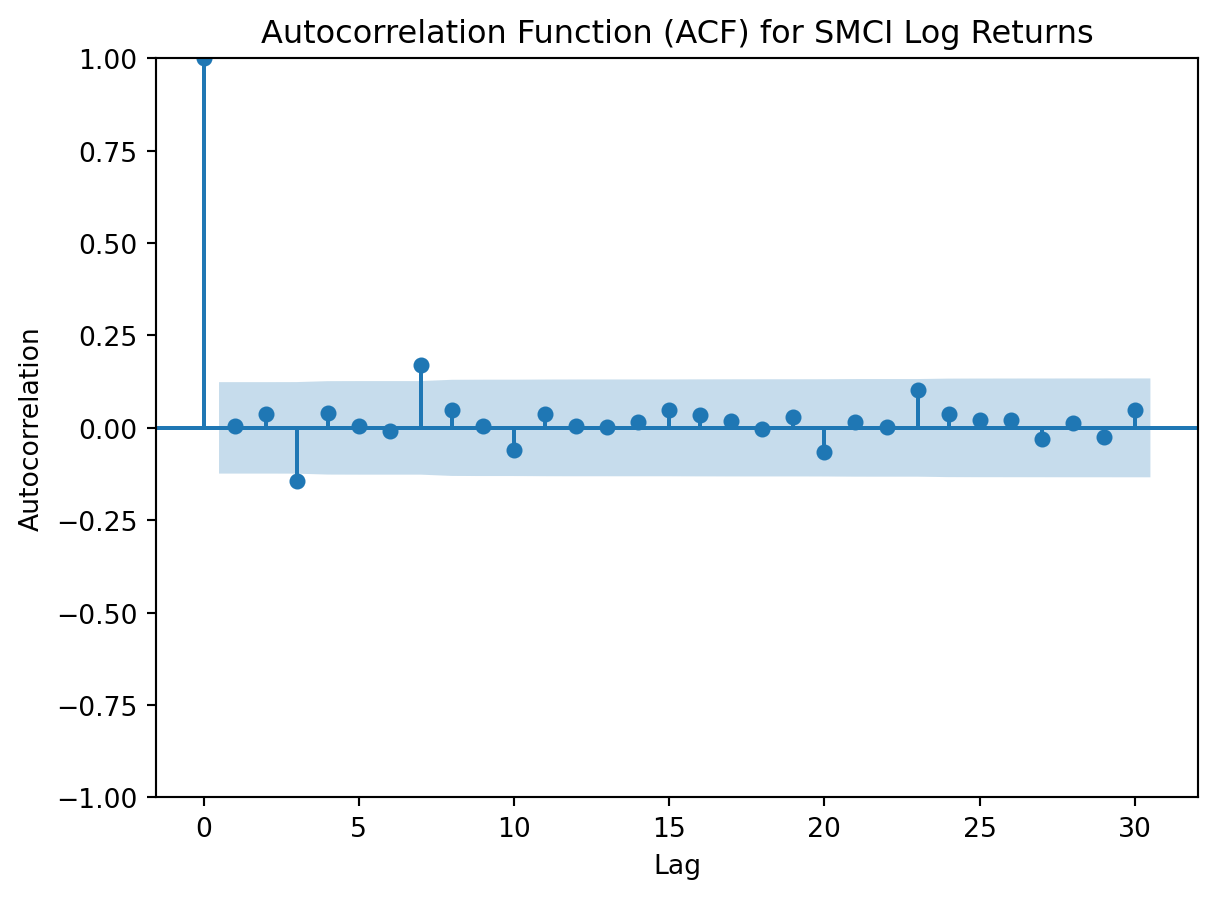

Statsmodels will grant us access to evaluating the datasets’ autocorrelations.

import statsmodels.api as sm

from statsmodels.graphics.tsaplots import plot_acf

from statsmodels.stats.diagnostic import acorr_ljungbox

# ACF plot for SBUX log return data

plt.figure(figsize=(10, 5))

plot_acf(SBUX['Log_Return'].dropna(), lags=30, alpha=0.05)

plt.title('Autocorrelation Function (ACF) for SBUX Log Returns')

plt.xlabel('Lag')

plt.ylabel('Autocorrelation')

plt.show()

# ACF plot for SMCI log return data

plt.figure(figsize=(10, 5))

plot_acf(SMCI['Log_Return'].dropna(), lags=30, alpha=0.05)

plt.title('Autocorrelation Function (ACF) for SMCI Log Returns')

plt.xlabel('Lag')

plt.ylabel('Autocorrelation')

plt.show()<Figure size 960x480 with 0 Axes>

<Figure size 960x480 with 0 Axes>

Both log returned stock prices have an autocorrelation function that feature none or minimal spikes in the autocorrelation coefficient. This indicates that autocorrelation is weak in the log yield data, and that any value is not strongly correlated with its previous value.

9.5 Forecasting using ARIMA

An auto-regressive model is a simple model that predicts future performance based on past performance. It is mainly used for forecasting when there is some correlation between values in a given time series and those that precede and succeed (back and forth).

An AR is a Linear Regression model that uses lagged variables as input. By indicating the input, the Linear Regression model can be easily built using the scikit-learn library. Statsmodels library provides autoregression model-specific functions where you must specify an appropriate lag value and train the model.

ARIMA (autoregressive integrated moving average) is a widely used approach for predicting stationary series. Building off of AR and ARMA - the latter of which cannot utilize non-stationary data - ARIMA can be used on both stationary and non-stationary data.

- AutoRegressive AR(p) - a regression model with lagged values of y, until p-th time in the past, as predictors. Here, p = the number of lagged observations in the model, ε is white noise at time t, c is a constant and φs are parameters.

\[ \hat{y}_t = c + \phi_1 \cdot y_{t-1} + \phi_2 \cdot y_{t-2} + \ldots + \phi_p \cdot y_{t-p} + \varepsilon_t \]

- Integrated I(d) - The difference is taken d times until the original series becomes stationary.

\[ B \cdot y_t = y_{t-1} \]

where B is considered the backshift operator. Thus, the first order difference is

\[ y_t^t = y_t - y_{t-1} = (1-B) \cdot y_t \]

and the dth order difference can be written as

\[ y_t^t = (1-B)^d \cdot y_t \]

- Moving average MA(q) - A moving average model uses a regression-like model on past forecast errors. Here, ε is white noise at time t, c is a constant, and θs are parameters

\[ \hat{y}_t = c + \theta_1 \cdot \epsilon_{t-1} + \theta_2 \cdot \epsilon_{t-2} + \ldots + \theta_q \cdot \epsilon_{t-q} \]

Bringing these parameters together results in the following ARIMA(p,d,q) model:

\[ \hat{y}_t^t = c + \phi_1 \cdot y_{t-1}^t + \phi_2 \cdot y_{t-2}^t + \ldots + \phi_p \cdot y_{t-p}^t + \theta_1 \cdot \epsilon_{t-1} + \theta_2 \cdot \epsilon_{t-2} + \ldots + \theta_q \cdot \epsilon_{t-q} + \epsilon_t \]

9.5.0.1 Using Training and Test Data with ARIMA

To illustrate the importance of transforming non-stationary data, we will split our data into traning and test data. We will forecast the test data using ARIMA on the original dataset, and compare root mean square errors with the log yield data set.

Statsmodels will allow us to access ARIMA, and sklearn will allow us to utilize root mean square errors.

from statsmodels.tsa.arima.model import ARIMA

from sklearn.metrics import mean_squared_error

# Function to split data into training and test sets

def train_test_split(data, test_size):

split_index = int(len(data) * (1 - test_size))

train_data, test_data = data[:split_index], data[split_index:]

return train_data, test_data

# Function to fit ARIMA model and forecast

def fit_arima_forecast(train_data, test_data, order):

# Fit ARIMA model

model = ARIMA(train_data, order=order)

fitted_model = model.fit()

# Forecast

forecast_values = fitted_model.forecast(steps=len(test_data))

return forecast_values

# Function to evaluate forecast performance

def evaluate_forecast(actual, forecast):

rmse = np.sqrt(mean_squared_error(actual, forecast))

return rmse

# Split data into training and test sets for SBUX

sbux_train, sbux_test = train_test_split(SBUX['Close'], test_size=0.2)

# Fit ARIMA model and forecast for SBUX

sbux_order = (30, 1, 1)

sbux_forecast = fit_arima_forecast(sbux_train, sbux_test, sbux_order)

# Evaluate forecast performance for SBUX

sbux_rmse = evaluate_forecast(sbux_test, sbux_forecast)

# Split data into training and test sets for SMCI

smci_train, smci_test = train_test_split(SMCI['Close'], test_size=0.2)

# Fit ARIMA model and forecast for SMCI

smci_order = (30, 1, 1)

smci_forecast = fit_arima_forecast(smci_train, smci_test, smci_order)

# Evaluate forecast performance for SMCI

smci_rmse = evaluate_forecast(smci_test, smci_forecast)

# Print RMSE for both SBUX and SMCI

print("RMSE for SBUX:", sbux_rmse)

print("RMSE for SMCI:", smci_rmse)

# Split data into training and test sets for SBUX Log_Return

sbux_diff_train, sbux_diff_test = train_test_split(

SBUX['Log_Return'].dropna(), test_size=0.2)

# Fit ARIMA model and forecast for SBUX Log_Return

sbux_diff_order = (30, 1, 1)

sbux_diff_forecast = fit_arima_forecast(sbux_diff_train, sbux_diff_test,

sbux_diff_order)

# Evaluate forecast performance for SBUX Log_Return

sbux_diff_rmse = evaluate_forecast(sbux_diff_test, sbux_diff_forecast)

# Split data into training and test sets for SMCI Log_Return

smci_diff_train, smci_diff_test = train_test_split(

SMCI['Log_Return'].dropna(), test_size=0.2)

# Fit ARIMA model and forecast for SMCI Log_Return

smci_diff_order = (30, 1, 1)

smci_diff_forecast = fit_arima_forecast(smci_diff_train, smci_diff_test,

smci_diff_order)

# Evaluate forecast performance for SMCI Log_Return

smci_diff_rmse = evaluate_forecast(smci_diff_test, smci_diff_forecast)

# Print RMSE for both SBUX and SMCI Log_Return

print("RMSE for SBUX Log Returns:", sbux_diff_rmse)

print("RMSE for SMCI Log Returns:", smci_diff_rmse)RMSE for SBUX: 5.203162195733355

RMSE for SMCI: 387.44378470841997

RMSE for SBUX Log Returns: 0.026718558204201322

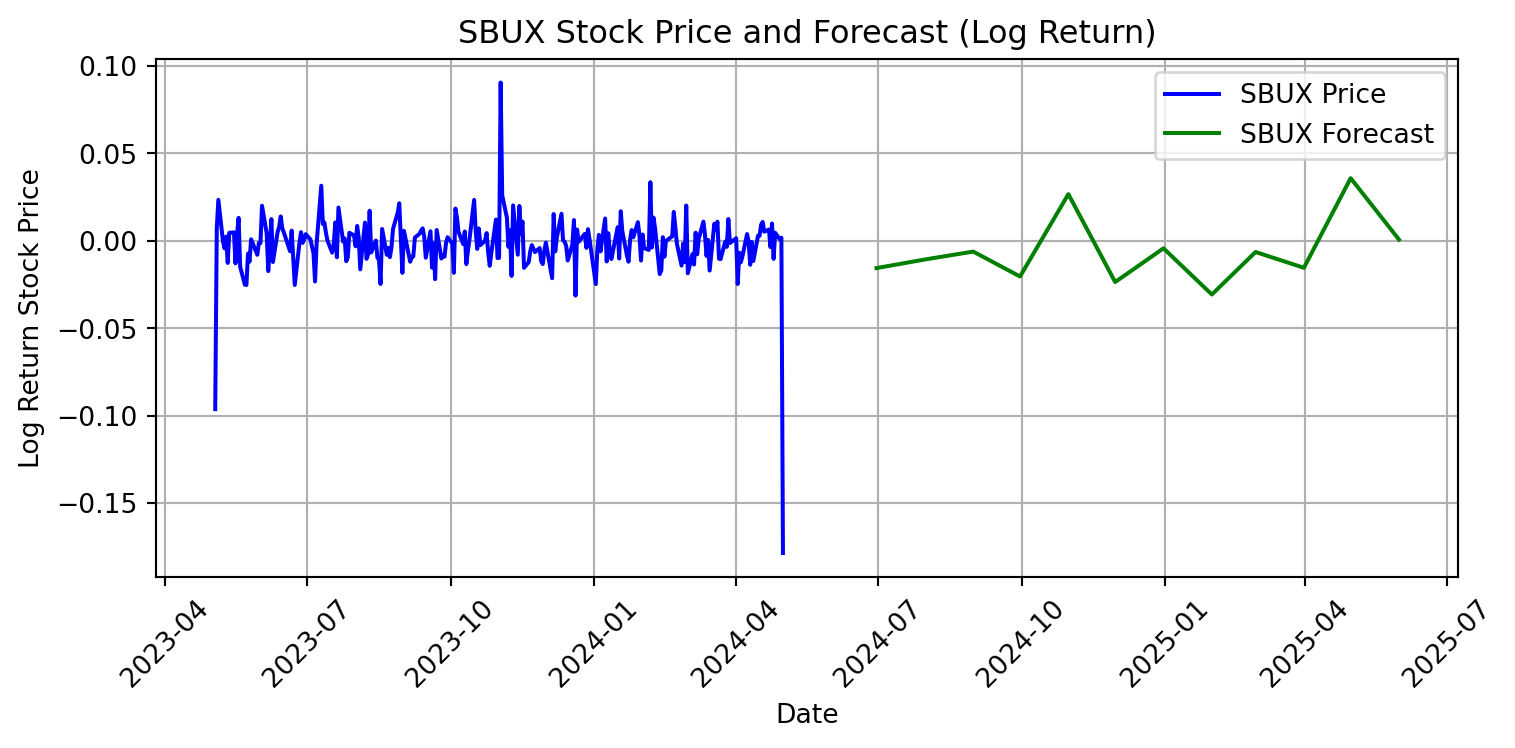

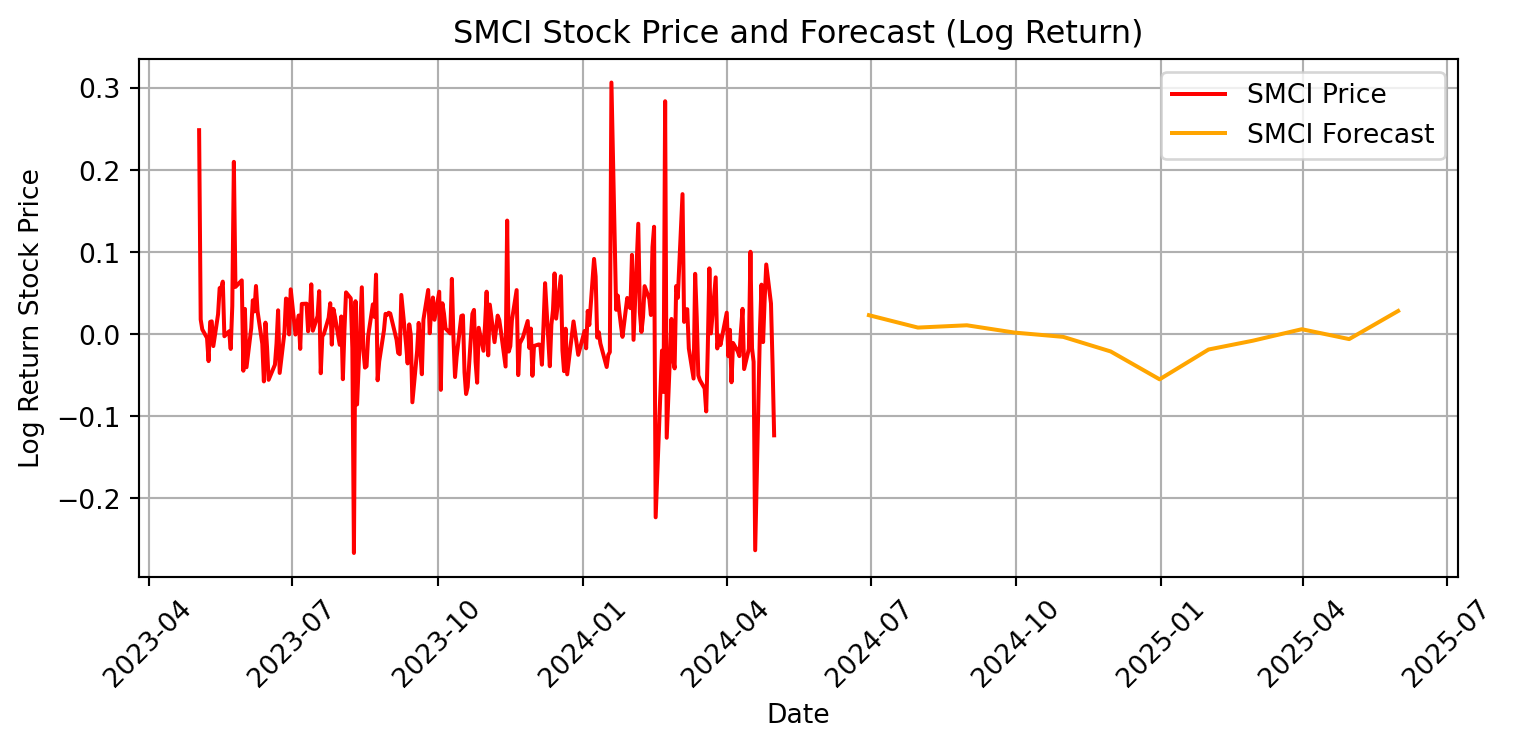

RMSE for SMCI Log Returns: 0.09062670255548778Finally, we can proceed with a forecast of these companies’ stock prices using ARIMA. Although ARIMA does not require stationary data, we can improve the accuracy of our model by using our detrended stationary stock prices.

# Set 'Date' column as index

SBUX.set_index('Date', inplace=True)

SMCI.set_index('Date', inplace=True)

# Define a function to fit ARIMA model and make forecast

def fit_arima_and_forecast(data, order):

model = ARIMA(data, order=order)

model_fit = model.fit()

forecast = model_fit.forecast(steps=12) # Forecast 12 months ahead

return forecast

# Fit ARIMA model and make forecast for SBUX

sbux_forecast = fit_arima_and_forecast(SBUX['Log_Return'], order=(30,1,1))

sbux_forecast_index = pd.date_range(start=SBUX.index[-1], periods=13,

freq='M')[1:] # Generate date range for forecast

# Fit ARIMA model and make forecast for SMCI

smci_forecast = fit_arima_and_forecast(SMCI['Log_Return'], order=(30,1,1))

smci_forecast_index = pd.date_range(start=SMCI.index[-1], periods=13, freq='M')[1:] # Generate date range for forecast

# Plot the forecasts

plt.figure(figsize=(8, 4))

plt.plot(SBUX.index, SBUX['Log_Return'], label='SBUX Price', color='blue')

plt.plot(sbux_forecast_index, sbux_forecast, label='SBUX Forecast',

color='green')

plt.xlabel('Date')

plt.ylabel('Log Return Stock Price')

plt.title('SBUX Stock Price and Forecast (Log Return)')

plt.legend()

plt.grid(True)

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

plt.figure(figsize=(8, 4))

plt.plot(SMCI.index, SMCI['Log_Return'], label='SMCI Price', color='red')

plt.plot(smci_forecast_index, smci_forecast, label='SMCI Forecast',

color='orange')

plt.xlabel('Date')

plt.ylabel('Log Return Stock Price')

plt.title('SMCI Stock Price and Forecast (Log Return)')

plt.legend()

plt.grid(True)

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

9.5.0.1.1 Interpretation of ARIMA

This model predicts greater volatility for Supermicro’s stock price than Starbucks’. The change in Starbucks’ stock price is not predicted to deviate from zero, while the change in Supermicro’s stock price is predicted to fluctuate. We have a neutral valuation of Starbucks’ stock, and would not recommend buying nor selling. However, since the forecasted log return stock are majority positive, we would recommend buying Supermicro stock. The ARIMA model indicates an a positive outlook and an expectation of future growth over the next 12 months.

9.5.1 Modeling Volatility With GARCH

A change in the variance or volatility over time can cause problems when modeling time series with classical methods like ARIMA. GARCH (Generalized Autoregressive Conditional Heteroskedasticity) models changes in variance in a time dependent data set. Consistent change in variance over time is called increasing or decreasing volatility. In time series where the variance is increasing in a systematic way, such as an increasing trend, this property of the series is called heteroskedasticity.

GARCH models the variance at a time step as a function of the residual errors from a mean process, while incorporating a moving average component. This allows the model to predict conditional change in variance over time.

The conditional variance is formulated as:

\[ \sigma^2_t = \alpha_0 + \alpha(B) \cdot \mu^2_t + \beta(B) \cdot \sigma^2_t \]

where \(\alpha(B) = \alpha_1 \cdot B + \ldots + \alpha_q \cdot B^q\) and \(\beta(B) = \beta_1 \cdot B + \ldots + \beta_p \cdot B^p\) are polynomials in the backshift operator B.

The GARCH(p,q) model contains two parameters:

- p: The number of lag variances included in the GARCH model.

- q: The number of lag residual errors included in the GARCH model.

The most frequently used heteroskedastic model with GARCH is GARCH(1,1), where \(p,q\) = 1. The formula for GARCH (1,1) is as follows:

\[ \sigma^2_t = \alpha_0 + \alpha_1 \cdot \mu^2_{t-1} + \beta_1 \cdot \sigma^2_{t-1} \]

Now, lets forecast variance at time t for a test set of both Starbucks and Supermicro stock prices. The arch package allows for us to complete these calculations.

from arch import arch_model

# Drop rows with NaN values in SBUX and SMCI dataframes

SBUX.dropna(inplace=True)

SMCI.dropna(inplace=True)

# Define GARCH models for SBUX and SMCI

sbux_model = arch_model(SBUX['Log_Return'], mean='Zero', vol='GARCH', p=1, q=1)

smci_model = arch_model(SMCI['Log_Return'], mean='Zero', vol='GARCH', p=1, q=1)

# Fit GARCH models

sbux_model_fit = sbux_model.fit()

smci_model_fit = smci_model.fit()

# Forecast the test set for SBUX

sbux_forecast = sbux_model_fit.forecast(horizon=len(SBUX['Log_Return']))

# Forecast the test set for SMCI

smci_forecast = smci_model_fit.forecast(horizon=len(SMCI['Log_Return']))

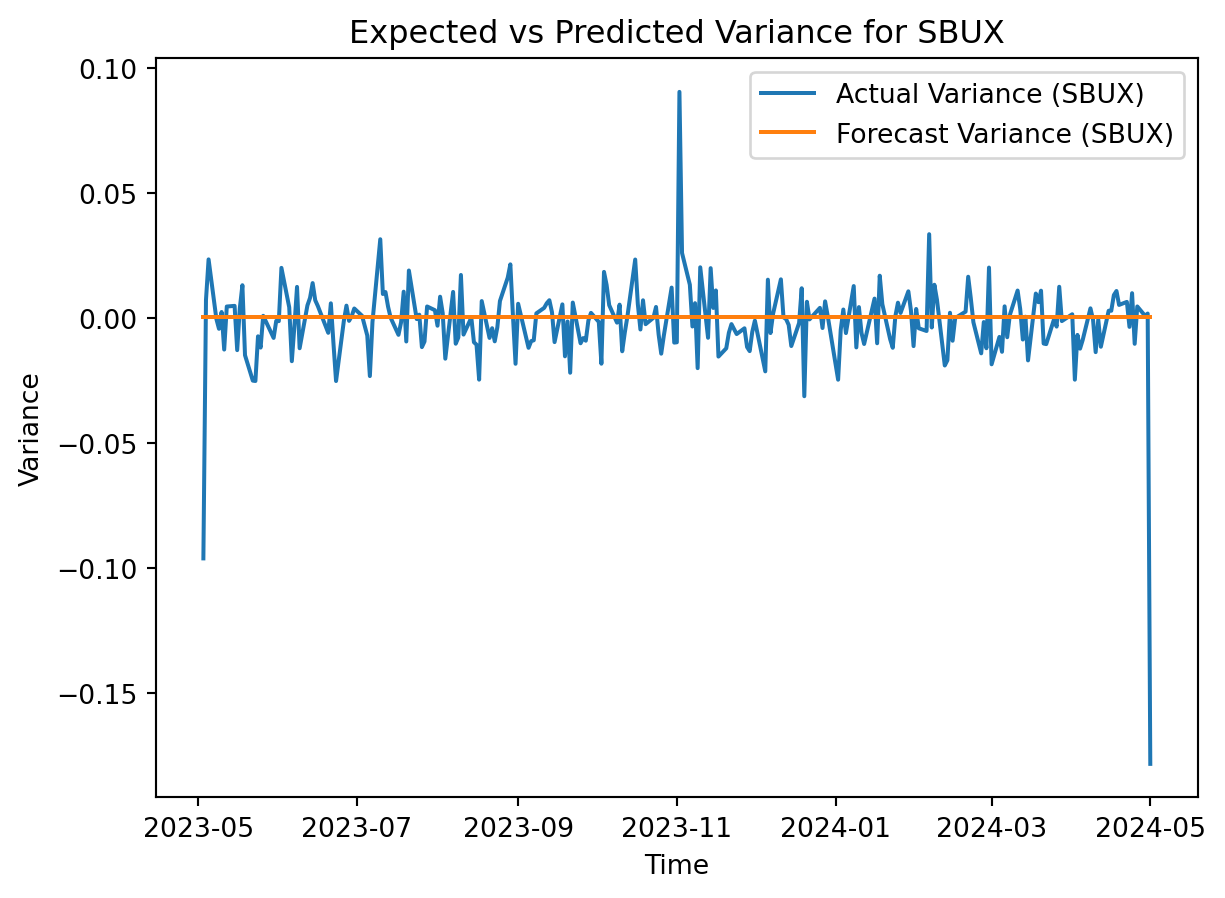

# Plot the actual variance and forecast variance for SBUX

plt.plot(SBUX.index, SBUX['Log_Return'], label='Actual Variance (SBUX)')

plt.plot(SBUX.index, sbux_forecast.variance.values[-1], label='Forecast Variance (SBUX)')

plt.title('Expected vs Predicted Variance for SBUX')

plt.xlabel('Time')

plt.ylabel('Variance')

plt.legend()

plt.show()

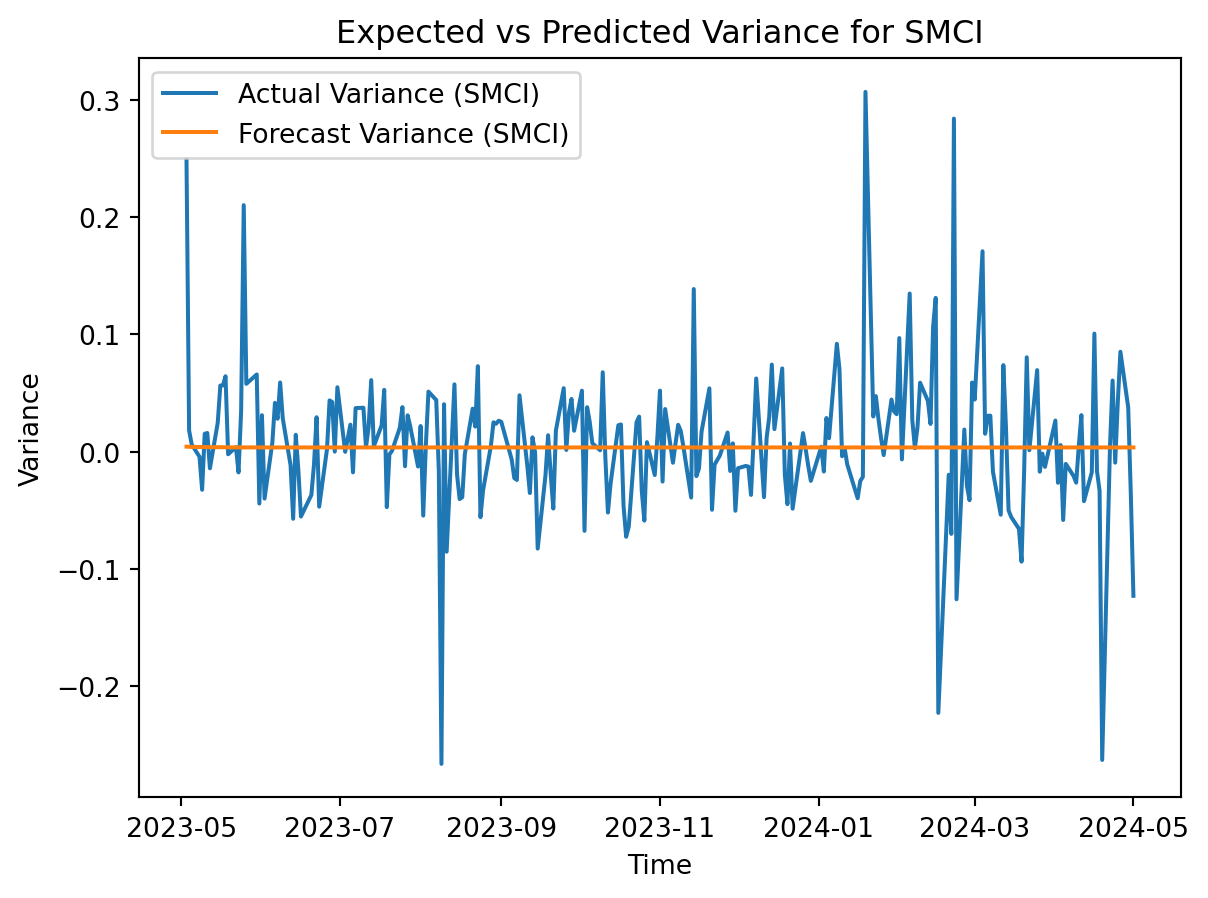

# Plot the actual variance and forecast variance for SMCI

plt.plot(SMCI.index, SMCI['Log_Return'], label='Actual Variance (SMCI)')

plt.plot(SMCI.index, smci_forecast.variance.values[-1], label='Forecast Variance (SMCI)')

plt.title('Expected vs Predicted Variance for SMCI')

plt.xlabel('Time')

plt.ylabel('Variance')

plt.legend()

plt.show()Iteration: 1, Func. Count: 5, Neg. LLF: 358097579.9412439

Iteration: 2, Func. Count: 11, Neg. LLF: -655.949119752052

Iteration: 3, Func. Count: 17, Neg. LLF: -455.66845988001626

Iteration: 4, Func. Count: 23, Neg. LLF: -633.7713503261562

Iteration: 5, Func. Count: 28, Neg. LLF: -662.4659498178196

Iteration: 6, Func. Count: 32, Neg. LLF: -662.4718784136544

Iteration: 7, Func. Count: 36, Neg. LLF: -662.4751595916471

Iteration: 8, Func. Count: 40, Neg. LLF: -662.486634024593

Iteration: 9, Func. Count: 44, Neg. LLF: -662.4894633348765

Iteration: 10, Func. Count: 48, Neg. LLF: -662.489604600355

Iteration: 11, Func. Count: 52, Neg. LLF: -305.2283082689668

Optimization terminated successfully (Exit mode 0)

Current function value: -662.4896063649699

Iterations: 12

Function evaluations: 58

Gradient evaluations: 11

Iteration: 1, Func. Count: 5, Neg. LLF: 51048.92008722303

Iteration: 2, Func. Count: 11, Neg. LLF: -272.5448314403104

Iteration: 3, Func. Count: 17, Neg. LLF: -286.46897203456945

Iteration: 4, Func. Count: 22, Neg. LLF: -346.94664830787303

Iteration: 5, Func. Count: 27, Neg. LLF: -328.37083263347984

Iteration: 6, Func. Count: 32, Neg. LLF: -349.0943859630313

Iteration: 7, Func. Count: 37, Neg. LLF: -349.1651727212498

Iteration: 8, Func. Count: 41, Neg. LLF: -349.1664669570813

Iteration: 9, Func. Count: 45, Neg. LLF: -349.1664804244107

Iteration: 10, Func. Count: 49, Neg. LLF: -349.1664810312767

Optimization terminated successfully (Exit mode 0)

Current function value: -349.1664810312767

Iterations: 10

Function evaluations: 49

Gradient evaluations: 10

GARCH shows that the forecasted variance is constant around zero for the logged returns. A higher volatility than expected for a stock is attactive for day trading, but far less so for long-term investments. Supermicro appears to be more volatile than Starbucks, so a day trader would likely be more interested in SMCI while an investor would be better off holding onto SBUX.

9.5.2 Conclusion

Conducting time series data analysis is a fundamental task encountered by data scientists across various domains. A strong grasp of tools and methodologies for analysis empowers data scientists to unveil underlying trends, anticipate future events, and inform decision-making processes effectively. Leveraging time series forecasting techniques enables the anticipation of future occurrences within the data, thus playing a pivotal role in decision-making processes.